Synthetic ETFs use

total return swaps to deliver the returns of an index. A swap is a contract with a financial institution that agrees to pay the return to the ETF in exchange for a fee.

Counterparty risk is the chance that the financial institution (usually a large global bank or securities dealer) defaults on its obligation. For example, there’s a small chance a counterparty could go bust during a financial crisis and is no longer able to pay the return.

This risk causes some investors to be wary of synthetic ETFs especially because regulators and the media put the products under the spotlight a few years ago. That scrutiny has significantly improved the level of protection offered by synthetic ETF providers, however. Here are the main features to look out for:

UCITS ETFs

European directives restrict an ETF’s exposure to any counterparty to a maximum of 10% of it’s Net Asset Value or NAV. The other 90% of the ETF’s value should be covered by collateral held on its behalf that would be sold to reimburse investors in the event of a default. Many ETFs are actually covered by collateral worth more than 90% of NAV in practice. More on this below.

Multiple counterparties

As with most things in life, diversification is a good way to spread the risk of failure by any one entity. Some synthetic ETF providers use their parent banks as a counterparty therefore it’s preferable to also have deals in place with unaffiliated counterparties to lessen potential conflicts of interest that could affect costs or collateral quality.

Swap resets

When an ETF’s index rises higher than the value of its collateral then investors are exposed to counterparty risk on the difference. However, the counterparty pays the ETF the difference in value when the swap agreement resets. That gain is invested in more collateral and counterparty risk is reduced to zero.

Similarly, if the collateral value rises fastest then the ETF pays the difference to the counterparty.

It follows then that the faster the swap resets when the ETF beats its collateral and the slower it resets when the collateral is ahead, the less counterparty risk is being run by investors.

Some swap agreements reset at thresholds before the maximum 10% of NAV is reached when the ETF is worth more than the collateral. Others will reset the difference daily. And in other cases, swap agreements will delay action when the ETF is due to pay out to the counterparty - increasing the value of collateral available to investors. The ETF provider should publish its policy in its prospectus.

Overcollateralisation

Some synthetic ETF providers routinely hold collateral valued at 100% to 120% of NAV. This provides a margin of safety in the event of a sale that makes it more likely the collateral will cover the full value of the ETF. A good ETF provider will review and publish the percentage of NAV collateralised daily via its website.

Quality of collateral

Collateral is composed of a basket of securities associated with the ETF. The more liquid and easy to value they are, the better it is for investors. Blue chip stocks and high credit quality government bonds are ideal.

This is because liquid, quality securities will be easier to sell in a crisis and are less likely to vary wildly in valuation. That means investors will get their money back more quickly and are less likely to take a haircut if the collateral sells below its pre-default valuation.

Unfunded vs funded swaps

The essential difference between the two types of swap is that the ETF directly holds its own collateral in the case of an unfunded swap. Whereas with a funded swap, the counterparty gathers the collateral and posts it in a segregated account with an independent custodian, where it is held on behalf of the ETF.

Unfunded vs funded swap model

![Unfunded vs funded swap model]()

Source: justETF.com

Regulators have voiced concern that this could potentially lead to a delay in the liquidation of collateral because the ETF provider can’t access it directly. However, funded swaps use legal arrangements known as a transfer of title or a pledge in order to ensure that collateral is readily available when needed.

A transfer of title means the collateral is treated as the property of the ETF and can be accessed without any further consent in the eventuality of a default. A pledge is slightly less straightforward because the collateral is held in the name of the counterparty for the benefit of the ETF.

Therefore transfer could be delayed if a bankruptcy administrator decided to freeze the counterparty’s assets.

Some ETF providers combine the two types in order to reduce costs.

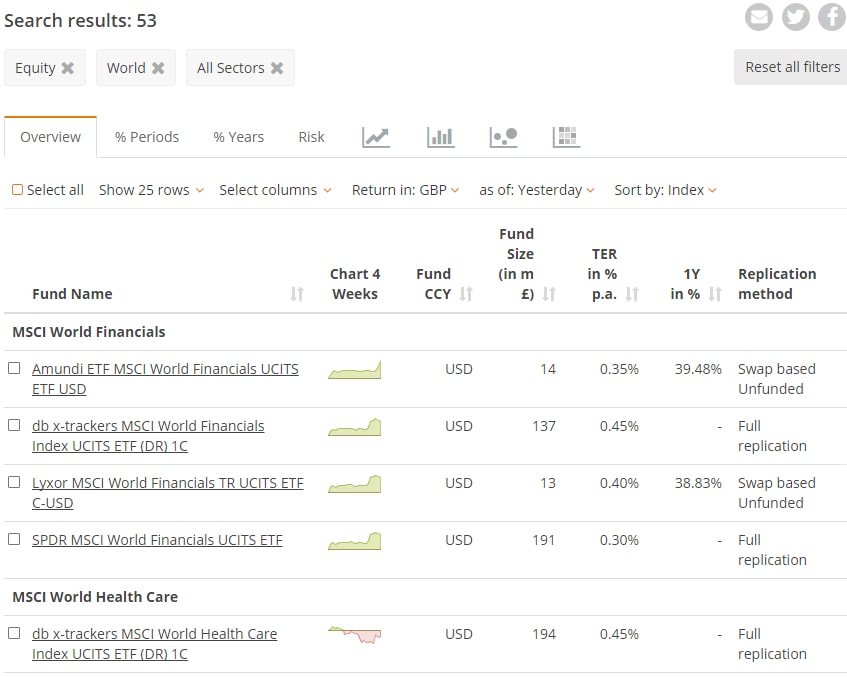

You can see whether an ETF uses a funded or unfunded swap using the

justETF screener. From the overview tab of a list of ETFs, click on the

drop-down in the variable column

on the far right which has Distribution policy as default.

Select

Replication method and you’ll see that synthetic ETFs are listed as Swap based funded or unfunded.

Synthetic ETFs in the ETF search

![Synthetic ETFs in the ETF search]()

Source: justETF.com

Transparency of ETF providers

Many providers now publish a list of their collateral holdings on a daily basis. They also disclose the level of collateralisation plus information on the number of counterparties and types of swap used for an individual ETF. You can use this to ensure that you are comfortable with the level of counterparty risk associated with any synthetic ETF.