Apple founder and visionary Steve Jobs used to say "There is one more thing" before presenting revolutionary innovations such as the iPhone or the iPad at the legendary Apple keynotes.

Admittedly: ETF providers certainly don't introduce new smartphones - but even in the ETF world, there are smaller and larger product revolutions from time to time. One of these this year is probably the new "hybrid replication". In this article, we take a closer look at what this is all about and who is the first to use it in their ETFs.

Hybrid replication: What is it?

Replication methods for ETFs could previously be divided into two basic variants: Physical and synthetic replication (although physical replication still has a sub-category with "optimised sampling").

As the name "hybrid replication" suggests, this new replication method is a mixture of physical and synthetic replication.

The ETF thus dynamically replicates its underlying index and can use both the one and the other variant to track its index. This can be particularly advantageous for broadly diversified global ETFs in order to optimally track the respective submarkets.

We will take a closer look at exactly how this works and the advantages and disadvantages of this method in a moment. But first, let's take a look at the basic differences between the various replication methods.

The difference: Physical, synthetic & hybrid replication of ETFs

Basically, each form of replication offers certain advantages and disadvantages. This is why there were previously three different replication methods that ETFs could use to replicate their corresponding index. Now, the hybrid replication method is being added:

(Full) physical replication is used to track easily accessible and highly liquid markets. ETFs on the DAX 40,FTSE 100 or S&P 500 are therefore often directly and fully replicated. The stocks included are among the largest stock corporations in the respective country and are easy to trade. In addition, the effort on the part of the ETF providers to buy a few dozen or a few hundred shares is limited.

Optimised sampling is mainly used for large indices with several thousand stock corporations. To track a global world equity index such as the MSCI ACWI IMI, for example, it is sufficient to buy a representative sample of around 3,500 shares instead of the approximately 9,000 shares contained in the index. This saves the ETF, and therefore you as an investor, money and is much more efficient.

Synthetic replication is preferably used for markets that are difficult to access, where the direct purchase of shares is far too expensive or made more difficult by regulatory conditions. Swap ETFs also offer structural advantages in some markets - for example in terms of withholding tax savings. More on this in a moment …

Hybrid replication is a combination of physical and synthetic replication. An ETF that uses hybrid replication can decide for itself within the ETF which markets it wants to replicate directly via physical replication and which markets are better included in the portfolio via swaps.

Comparison of ETF replication methods

Physical (complete)

Physical (sampling)

Synthetic

Hybrid

Replication method

Full replication

Sampling

Swap-based

Mixture of physical and synthetic replication

ETF description

The index is replicated 1:1 in the ETF

The ETF holds a representative selection of index stocks

Index replication takes place via a swap transaction

ETF holds shares both directly and via swap partners

Underlying assets

Stocks, bonds

Stocks, bonds

Stocks, bonds, commodity indices, money market indices, short and leverage indices

1Stocks

Typical characteristics of the index components

Liquid securities

(Partially) illiquid securities

Liquid and illiquid securities, investment restrictions (trading restrictions, taxation), various time zones

Liquid and illiquid securities, investment restrictions (trading restrictions, taxation), different time zones

Source: justETF Research; as at 17/12/2024 1Hybrid replicating ETFs are currently only available on equity indices

How does hybrid replication work with ETFs?

The strengths of the new replication method are particularly evident in broadly diversified equity indices such as the MSCI ACWI or the FTSE All World. The aim of the hybrid replication method is to combine the advantages of physical replication with those of the synthetic replication method. How does this work in practice?

One example is swap ETFs on the S&P 500, which have a decisive advantage over their physically replicating siblings - there is no withholding tax on dividends.

How so? While physically replicating ETFs have to pay at least 15 % withholding tax on US dividends as they invest directly in US equities, a swap ETF simply swaps the return of the index with a corresponding financial institution (the counterparty or swap partner).

No US equities are required in the ETF's carrier portfolio. And where no US shares are purchased directly, no withholding tax is incurred. This is also the reason why synthetic ETFs on the S&P 500 have slightly higher long-term returns than physical S&P 500 ETFs.

Comparison: Physical (orange) vs. synthetic (blue) S&P 500 ETF

Source: justETF Research; as of 16/12/2024

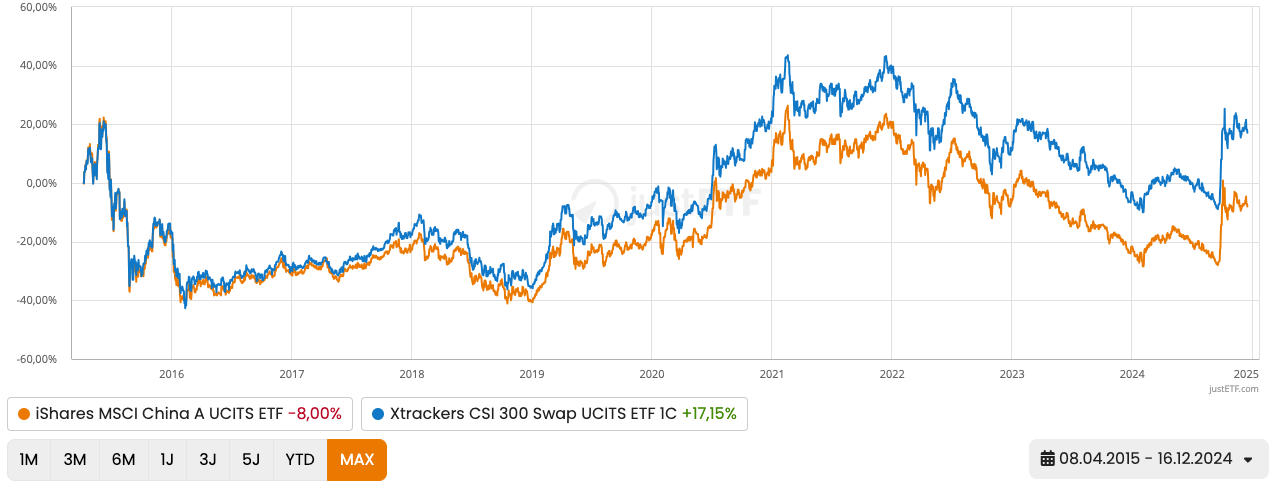

With synthetic ETFs, investors can also benefit from a unique structural dynamic in the Chinese local A-share market. This particular equity market is highly restricted or regulated and at the same time offers an attractive environment for professional investors (e.g. hedge funds) pursuing market-neutral strategies.

However, these investors often only have limited access, for example for short selling (= taking short positions) to hedge their market risk. As a result, these market participants are prepared to pay the swap counterparties of synthetic ETFs (usually large banks) a premium on the short exposure to which the counterparties are exposed.

This additional premium is partially passed on to investors in synthetic A-share ETFs and has historically led to outperformance. The premium may fluctuate over time and is primarily dependent on demand from these market participants.

Comparison: Physical (orange) vs. synthetic (blue) China A-Share ETF

Source: justETF Research; as of 17/12/2024

One disadvantage of a synthetic ETF compared to a physically replicating ETF is that it may not be able to carry out securities lending if it does not hold the required securities in its portfolio. Many swap ETFs do not use securities lending anyway. However, this is a common means for ETFs to generate additional income for fund investors.

Counterparty risk with swap ETFs

With swap ETFs, the so-called counterparty risk is often cited as a major disadvantage. But is the risk of swap ETFs really that great? The short answer is: No. Because:

As a rule, both the ETF and the swap counterparty hold collateral in the form of liquid securities.

This collateral must always physically collateralise at least 90 % of the net asset value (NAV). Or the other way round: the counterparty risk is capped at a maximum of 10 % of the fund assets and is balanced daily.

In practice, synthetic ETFs are often over-collateralised (collateral > NAV) and you can view the collateral portfolio and the selected swap partners transparently at any time on the websites of many ETF providers.

So far, European investors have not suffered any losses due to swap counterparty risk - even in times of the most severe crises (e.g. 2008 & 2020).

And this is where the hybrid replication method comes into play - because it can be used, for example, to synthetically replicate the US market "withholding tax-optimised" in a global ETF, while the European or Japanese equity market is physically replicated "securities lending-compliant". The result is actually the combination of "the best of both worlds" - because the respective ETF can optimally map the corresponding submarkets depending on the structural conditions and thus enable a minimally higher return for you as an ETF investor.

Important: Synthetic ETFs can also lend securities from the carrier portfolio. It then depends on which securities in the carrier portfolio are in demand and how. With higher demand or less liquidity, for example, higher returns can typically be achieved than with highly liquid securities. You can find out more about this in our article on securities lending with ETFs.

Which ETFs use the new hybrid replication method?

At the start, only one provider is offering an ETF on the MSCI ACWI with hybrid replication: Xtrackers. The Frankfurt-based asset manager has teamed up with online broker Scalable Capital to launch a global ETF.