If you've ever felt overwhelmed by the choices involved in investing - what to buy, when to rebalance, how much risk to take - you're not alone. Many investors want a simple, hands-off way to grow their wealth over time, especially if they're saving for a momentous future goal like retirement, buying a home, or a child’s university education.

Enter target date ETFs. These multi-asset investments are designed to steadily grow your capital, then gradually reduce risk as you approach the time you’ll need the money - the “target date year”.

Mutual fund versions of these products have been helping investors reach their objectives for years. Now ETF providers are joining the fray. iShares LifePath range arrived Stateside in 2023, and Amundi launched their Lifecycle family for European investors in 2025.

Without question, target date ETFs are a very welcome innovation, so let’s unpack what they are, how they work, and whether they could be useful for you.

What is a target date ETF?

A target date ETF is a ready-made portfolio that automatically adjusts its mix of assets - typically stocks and bonds - as a specific date approaches. That “target date” is usually linked to a financial goal, most commonly retirement, but it could just as easily be the year you plan to buy a home, or fund a child’s university costs.

The product starts off growth-focused (mainly stocks), then gradually shifts towards less risky assets (bonds and cash) as the date approaches - a process known as the glide path.

The glide path: how risk fades over time

Target-date glide paths are founded on well-established investing wisdom:

Most people can afford to take more risk (in search of higher growth) when they’re relatively young, or many years from reaching their objective.

Conversely, older investors, or people nearing their target, should increasingly focus on wealth preservation above growth.

Why? Because when you start out, your early investing contributions are a small proportion of your likely future earnings and later-life wealth.

Thus, a large stock allocation makes sense at this stage because you have much to gain and little to lose.

But eventually you’ll reach a crossover point.

Beyond that threshold, your accumulated investments will amount to an increasingly high proportion of your target number.

While your remaining working years will be fewer, reducing your financial capacity to make up any lost ground.

At this stage of life, you have less to gain and much more to lose.

To dramatically lower the odds of a serious loss occurring, target date ETFs incrementally replace volatile equities with more stable bonds and cash.

This risk-management technique reduces the chance of a major setback and thus protects the wealth you’ve built.

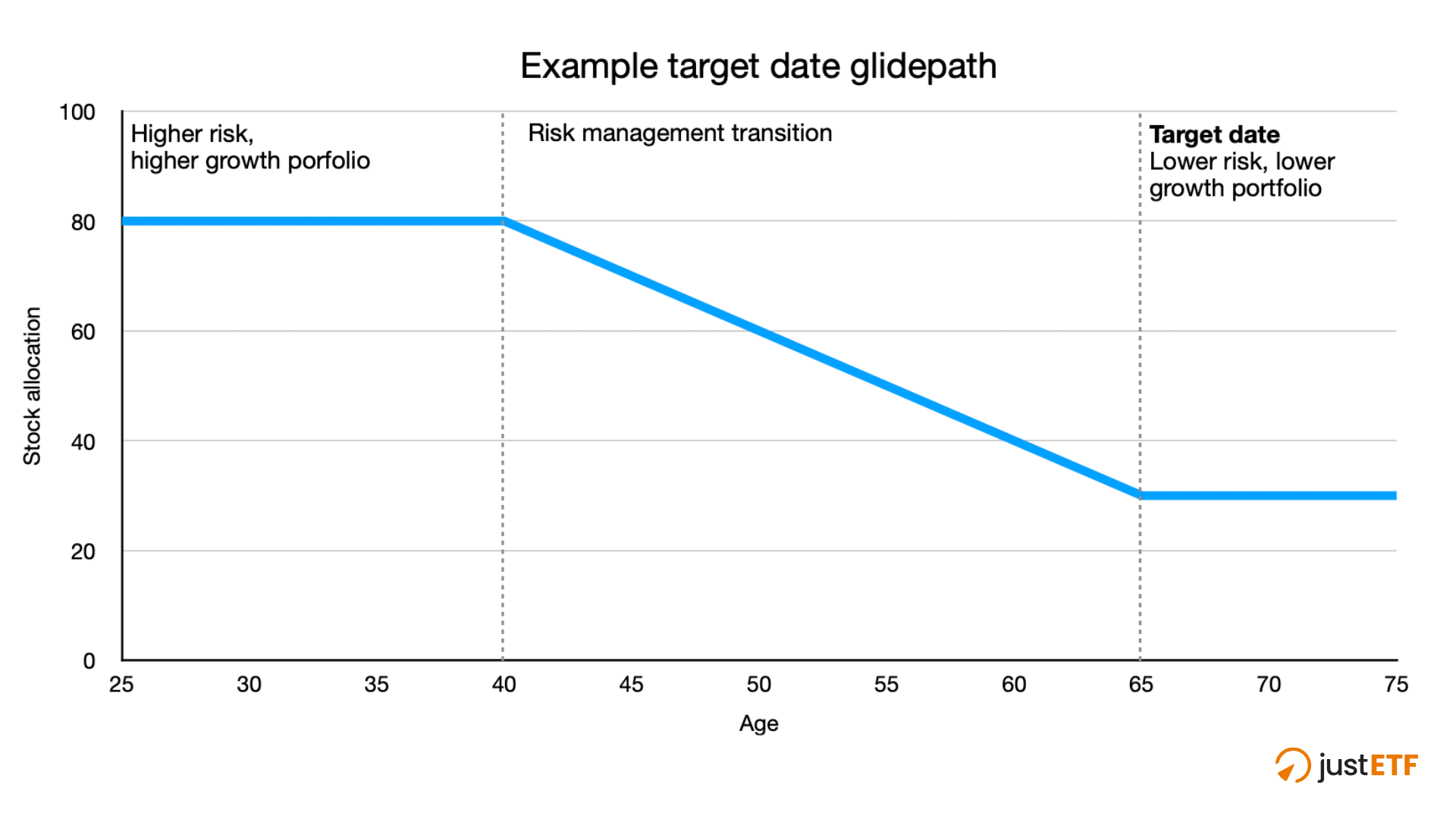

Here’s a simplified example of how a classic glide path looks :

Example target date glidepath

Source: justETF Research; Generic target date glidepath not based on a specific investment product.

The blue line shows how the equities allocation declines as the target date approaches.

The remainder of the allocation is replaced by less risky assets such as bonds and cash. The downside of these assets is typically lower growth rates than stocks.

But they earn their keep by lowering portfolio volatility and being more likely to hold their value during economic turbulence. The older you get, the more important that becomes.

Once the target date is reached, the product’s asset allocation either remains static, or its shares are redeemed. If an ETF’s shares are redeemed, then each investor has their capital returned to them as cash, to spend or reinvest as they see fit.

Of course, target date ETFs can be bought and sold at any time, just like normal ETFs. You aren’t locked into the product, nor committed to the glide path if you want to cash out early.

In fact, selling up is precisely the right move if you enjoy dream returns and hit your target figure ahead of time.

Extremely low volatility: best wealth preserver at journey’s end

Bonds and money market holdings should be denominated in your local currency (or hedged to your currency) to guard against currency risk.

This approach means your money is spread across different countries, sectors, and asset classes to cope with a range of economic conditions.

Investment selection and rebalancing is automatically handled for you. You do not have to get involved - which is the joy of a target date ETF.

How to choose a target date ETF

The year a target date ETF completes its glide path journey is featured in its name.

If you like the overall product offering, then you simply pick the iteration which most closely corresponds with the year you plan to reach your objective.

To take a real example, if you’d like to retire in 2040 then you’d pick the Amundi Lifecycle 2039 UCITS ETF.

Or perhaps you’d like to invest to pay for your child’s university fees in 2035? Then it’s the Amundi Lifecycle 2036 UCITS ETF for you.

Currently, Amundi’s Lifecycle range is staggered in three-year intervals like this:

If European investors embrace target date ETFs, then you can assume Amundi will release more Lifecycle products to cover the 2040s and beyond. Other providers will likely enter the market too.

It’s absolutely fine to have a two to three year gap between your intended date and the ETF’s headline target date. Investing is not an exact science, so there’s no need to align precisely to the year quoted in the product name.

Remember too, it’s the year you plan to complete your goal that counts, not the goal itself. Regardless of the amount and the objective at stake, the purpose of a target date ETF is to reduce your downside risk as your deadline approaches.

What you need to monitor

Target date ETFs may operate smoothly on autopilot, but you still need to keep an eye on them.

They do not guarantee that you’ll reach your investment goal by a specific time, nor are they immune to market shocks.

For example, while high-quality government bonds are the best asset for countering stock market contractions, they do not always work on cue.

Stocks and bonds can sometimes fall together. And both assets are vulnerable to fast-rising inflation, as we saw in 2022.

So while you can happily leave your target date investments alone for a year or two, you should check in from time to time.

As a minimum, adjust your investment cash in line with annual inflation to maintain the purchasing power of your contributions.

And be prepared to invest more, or for longer, if you're unlucky enough to experience a poor run of returns. This is the best way to reach your number if you’re worried about falling short.

The wrong way is to load up on ever riskier assets that could derail your plans if you suffer further misfortune.

On the other hand, think seriously about selling up if you enjoy wonderful investments returns and reach your destination early. Pushing your luck can put what you have at risk.

Finally, use a realistic rate of return, keyed to your target date ETF’s asset allocation, when calculating how long it may take you to hit your number in the first place.

Achieving that target is a function of the amount you contribute, the number of years you invest, and the overall return you achieve.

The first two numbers are within your circle of control, but future returns are inherently unpredictable.

Pros of target date ETFs

Simplicity: One investment does it all - asset allocation, diversification, and risk management.

Hands-off investing: The ETF adjusts automatically as your goal gets closer. No need to trade or rethink allocations yourself.

Behavioural benefits: By taking decision-making out of your hands, target date ETFs can reduce the temptation to time the market or panic-sell during downturns.

Low cost: Target date products typically provide battle-tested passive investing strategies for a competitive fee.

Cons of target date ETFs

Not personalised: The glide path is based on a "typical" investor - but your circumstances might be different. You might have a higher or lower risk tolerance, for example.

One-size-fits-all glide path: Products may de-risk too quickly or too slowly for your needs. You may end up being too conservative or too exposed to risk near your goal relative to your personal preference.

Cost gap: While target date ETFs are low cost (Amundi’s Lifecycle ETFs have a 0.18 % TER), you can manage your own ETF portfolio for less.

Hard to adjust mid-journey: You can’t easily tweak the asset mix. If your plans change, you may need to sell the fund and reinvest elsewhere.

Tax complications: You can’t tax-loss harvest or prioritise which assets to put in your tax shelters. This may be tax inefficient if your target date product is held in taxable accounts.

Bottom line: Are target date ETFs right for you?

If you have a clear time horizon

Want automatic risk adjustment over time

Prefer to outsource investment decisions

But target date ETFs are not perfect - not least because there’s only one range available in Europe right now.

Moreover, if you want to customise your strategy, add different assets, or have unpredictable timelines, then a DIY approach might suit you better.

Ultimately, target date funds are a powerful tool - and like all tools, they work best when matched to the right job.