Many investors regard companies that pay high dividends as solid and profitable. Nevertheless, the major stock indices are dominated by the global growth companies of the digital economy, which prefer to invest their earnings into further expansion.

Companies that work with proven business models and regularly distribute large portions of their profits to investors through dividends have been, therefore, less in the focus of investors’ attention, but offer attractive opportunities for an income portfolio. In 2022, the world's largest 1,200 companies paid out around USD 1.56 trillion in dividends.

High income from dividends and interest can provide a passive source of income. Without any trades, your investment will pay you adequately. While traditional ways of investing like fixed income ETFs hardly generate income due to capital market developments, high-dividend equity strategies offer alternatives. ETFs provide a simple and inexpensive way to invest in dividend strategies. There is a wide selection: You will find ETFs with dividend optimised strategies in almost every developed equity market.

Finding the right passive source of income

Some private investors buy individual stocks for their portfolio in order to generate income from dividend distributions. They believe that they are able to pick the stocks with the best dividend outcomes. In reality, however, this strategy often results in disappointment.

In addition, you will not only find high-dividend securities in your home market, but you will also have to trade on foreign stock exchanges resulting in higher commissions. Besides, diversification is limited. ETFs and funds can invest in a lot more different companies and thus reduce the investment risk by diversification.

Actively managed dividend funds represent a second alternative that can offer a diversification comparable to the market index. A handful of fund managers can also look back on a better performance than their benchmark index (outperformance of the benchmark). However, most active funds are unable to outperform the market. Regardless of whether the manager is doing a good or a bad job, you as an investor have to pay substantial management fees each year. On top of this, you need to consider the transaction costs within the fund if the fund manager trades a lot.

ETFs: The best way to income from dividends

We believe a portfolio of well-chosen ETFs offers a superior income solution. With one or even more ETFs, you diversify your capital into many individual investments, chosen and weighted by the index provider.

Instead of an active fund manager, the underlying index of the ETF selects the stocks with the highest dividends. In this way, you can implement an income portfolio far more cost-efficiently, with less risk and easier maintenance. Lower costs mean more income for you to further invest or to spend.

Global ETF investment

Discover the best ETFs on the MSCI World Index in our investment guide!

ETF pay-outs: The right ETFs for your dividend strategy

As an investor in ETFs, you always benefit from the dividend payments of the companies you invest in. Depending on whether you prefer distributing or accumulating ETFs, the returns are paid out or reinvested. Therefore, distributing ETFs are a good fit for an income portfolio. Common market indices such as the MSCI World already provide a good dividend income of around 2%.

In addition to the classic market indices, there are also specialised dividend ETFs are available. The dividend indices used by these ETFs select and weight their stocks according to their dividend yields of previous periods. There is a wide choice for such ETFs is wide and allows you to benefit from high-dividend companies from all over the world, specific regions or even single countries.

But by focusing on dividends, you are taking a risk in comparison to a market index: companies with high dividends usually have conventional business models that may run the risk of being replaced by modern technology and service giants.

Furthermore, companies that pay high dividends do not necessarily achieve high profits. Dividends can also be paid out of the company's assets thereby eroding the company’s capital stock. In addition, many companies like to buy back shares instead of distributing profits in the form of dividends.

However, the methodologies of the index providers differ considerably and are, therefore, exposed to these risks at varying degrees. It is advisable to take a closer look at the index methodologies before investing. Our introduction to global dividend stocks, European dividend stocks and German dividend stocks gives you a quick yet detailed overview.

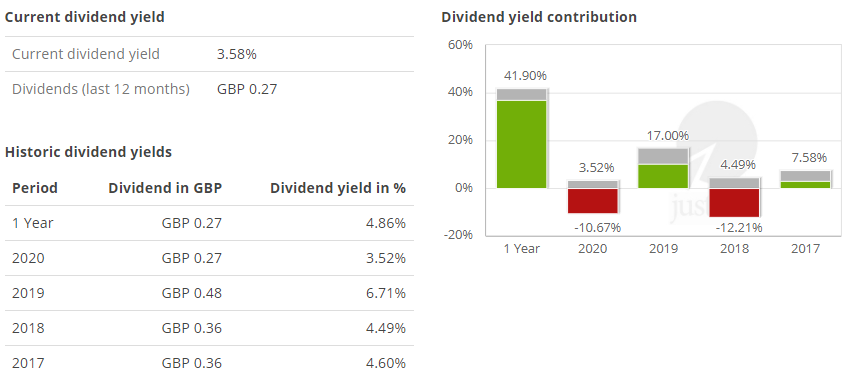

ETFs with dividend payments: How to measure the dividend yield of an ETF

The dividend yield is another critical factor in determining an ETF's potential for income. It refers to the distribution of an ETF in relation to its price.

Dividend yield = Annual dividends per share/cost per share

If an ETF pays 75p as a dividend and it costs 1800p to buy, the dividend yield is:

75p / 1800p = 4.17%

Do you rather take a look into the past or into the future? Both are possible: The historical payout yield takes the dividends of the last 12 months into account in relation to the share price 12 months ago. But it can also be calculated on an annual basis. Since prices fluctuate, the absolute annual payout amount often allows for a better measure of stability.

The current distribution yield, on the other hand, provides a forecast for the coming 12 months and compares the distributions of the past 12 months with the current stock market price. If you make an investment decision today, you should also be concerned about future returns and take the current distribution yield into account. Remember, however, that for equities this is always an estimate or indication, but not a guarantee. Nevertheless, the current dividend yield is a good entry-point for searching for interesting ETFs for an income portfolio. Our Top 50 lists of ETFs with the highest dividend yield will give you a first impression.

Let the hunt for dividends begin

Start a comparison of dividend yields with the now. In our ETF search site and on the ETF profiles you will find historical and current distribution yields of ETFs and their annual payments versus performance.

Information on distributions on ETF profiles at justETF

Source: justETF Research; as of 01/04/2021

Stay up to date

Free English newsletter including the latest news & knowledge about investing in ETFs.