People invest in bonds mostly because they add a welcome dose of stability to our portfolios. But you can still make large gains and losses on bonds and interest rate risk helps explain why.

Bond interest rates are the result of supply and demand for each and every bond on the market. That means each bond has its own interest rate (yield) which fluctuates constantly as the market changes its view in response to inflation prospects, the economic outlook, credit risk and the animal spirits of investors.

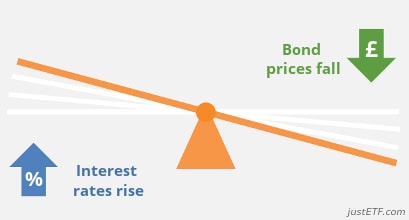

As official interest rates move, the price of bonds moves too, as surely as one end of a see-saw rises when the other end dips.

Effect of interest rates on bond prices

- When interest rates fall, bond prices rise

- When interest rates rise, bond prices fall

This relationship is a mathematical certainty because otherwise the bond market would freeze.

The reason is simple: new bonds are issued with a coupon that matches the current interest rate. (A bond’s coupon is simply the interest rate it pays on its face value.)

For example, a freshly minted 5-year

government bond is offered to investors with a 3% coupon.

The bond pays out 3% on its face value of £100 for every year of its existence. In other words, annual interest of £3 is due until the bond matures in 5 years time – whereupon the government pays back the £100 face value on the maturity date.

But what if you own an older government bond that was issued when interest rates were lower? Your bond only pays 2% coupon annually and still has 5 years left until maturity. Aside from its lower interest rate payment, your older bond is pretty much identical to the new 3% bonds. Not a winner.

In a world of 3% bonds, who would be mad enough to pay £100 for your 2% bond? No-one, that’s who. So, if you need to sell your 2% bond, you will have to drop its price to the point where it can compete with new bonds.

And that price is £95.24

You take a capital loss of £4.76 on the original £100 you invested in the bond. You’re not happy but your buyer will at least make the trade because your discount bond gives them a yield to maturity of 3% over 5 years.

That’s because your bond’s 2% payments plus the capital gain they make when the government pays them the bond’s £100 face value in 5 years, matches the 3% they can earn buying a new bond for £100 and holding that for 5 years.

The same thing works in reverse. If interest rates fall but you hold older bonds that pay out high rates of interest, then you can now sell them at a higher price because of the inherent value embedded in their coupon.

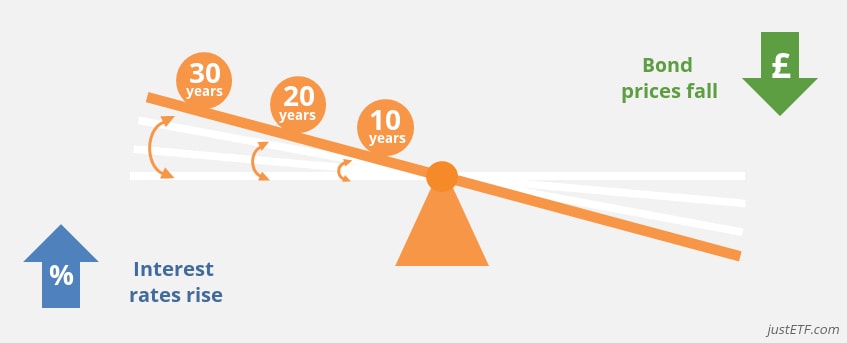

Effect of bond maturity on bond prices

![Effect of bond maturity on bond prices]()

The maturity of a bond is the countdown to the date that its face value is paid back. A 10-year government bond with a face value of £100 matures in a decade’s time when Her Majesty’s Treasury stumps up the last interest payment and £100 to clear the debt.

In 9 years time, that bond will now be a 1-year government bond, but its coupon rate and face value are fixed over its lifetime. That is why bond investing is sometimes referred to as fixed income investing.

Naturally, it’s no surprise to learn that the market demands a higher yield from 10-year bonds than it does for their 1-year equivalents.

Imagine how comfortable you would be with loaning somebody a large amount of cash for a decade instead of 1 year. What if you need the money back fast? What if that person disappears? What if inflation runs riot and destroys the value of the loan?

The bond market similarly demands a higher reward for longer loans to compensate for the risks of an uncertain world. Some bonds don’t mature until 20 or even 50 years in the future. Remember that the bond’s cashflows – its interest payments and face value – don’t change. If inflation jumps, then it will damage more cashflows on a bond paying out for the next 20 years than an equivalent bond that has only a couple of interest payments left before it matures in a year’s time.

Long-term bonds must offer higher interest rates to offset this risk, and you can see how this plays out in the higher average yields of long-term

bond ETFs versus their short-term counterparts.

The impact of changes on future cashflows also means that fluctuating interest rates affect long-term bonds more than short ones.

A rise in interest rates inflicts a bigger capital loss on a long-term bond because more of its forthcoming interest payments are now inferior to the yield you can earn on a new bond. Again, short-term bond prices are less affected because they compensate buyers for the shortfall on fewer interest payments.

The counter-punch is that long-term bond prices gain much more from interest rate falls.

Bond duration

How much will the value of your bond ETF rise or fall in response to interest rate shifts? The number to look out for is average duration.

Duration tells you roughly the size of the capital gain or loss you can expect in response to a 1% change in interest rates. The chart below shows how this affects bond ETFs of different durations.

Price change of a bond etf if interest rates increase by 1%

![Price change of a bond etf if interest rates increase by 1%]()

Note: Exemplary illustration of the effects of an increasing interest rate

- A duration 2 ETF drops about 2% in value if interest rates move up by 1%. It would gain 2% if rates fell by 1%.

- A duration 6 ETF drops about 6% in value if interest rates move up by 1%. It would gain 6% if rates fell by 1%.

Essentially, you multiply the duration number by the interest rate change to find out the approximate gain or loss.

Duration also tells you roughly how long it will take your bond ETF to recover from any loss.

A duration 2 ETF takes 2 years to recover while a duration 6 ETF takes, you guessed it, 6 years.

The recovery occurs because the ETF will invest in new, higher yielding bonds after the rise. Eventually that stronger flow of interest payments wipes out the capital loss – as long as you reinvest all your interest payments along the way.

Again, this process works in reverse. The capital gain of a duration 2 ETF will be eroded to nothing by weaker interest payments paid over the 2 years following an interest rate drop.

You can find an ETF’s average duration along with its average yield and coupon on its factsheet.

You’ll notice that low duration numbers are associated with short-term bond ETFs. Duration rises as ETFs hold bonds of greater maturity so you can quickly gauge the impact of interest rate changes on different products.

Remember that duration isn’t a perfect measure of the real world – because interest rates don’t uniformly affect all bonds – but it’s still a useful rule of thumb.

Whereas duration falls for individual bonds as their cashflows run down, a bond ETF’s manager will sell-off shorter-term holdings in order to maintain a steady duration.

Therefore, investors who expect to sell within a few years may well want to stick with short-term, low average duration ETFs. That minimises the impact of selling a portion of your holdings at a loss after an interest rate rise.

Whereas investors who will be accumulating for many years to come can ignore the fluctuations in bond prices and invest in a longer duration ETF that will reward you with greater yield.

Be careful not to invest in an ETF with a duration that’s longer than your time horizon and bear in mind that long-term products could suffer large losses if interest rates climb from their historic lows. If you’re in any doubt, then remember that short duration bond ETFs expose you to the least interest rate risk.