How much money would you loan to somebody if you didn’t trust them to pay it back? Not very much probably. Certainly not enough to put your financial security at risk.

It’s this question of trust that lies at the heart of the bond markets. How confident can you be that a country or a company will pay your money back with interest? The truth is that you can’t be 100% certain that a bond issuer will pay as promised. There’s no debt collection agency that can force a country to cough up and a company may run out of cash. This is the nature of credit risk.

Failure to pay bondholders in full is known as a default. A default can be as catastrophic as a total wipeout. This famously happened to Russian bondholders in 1917 when the Communist Government refused to repay Tsarist-era debt.

Thankfully total bond losses are rare and defaults usually mean that a bond issuer:

- Doesn’t make an interest payment or multiple interest payments.

- Doesn’t repay the face value of the bond.

- Does repay the bond but at a lower amount or over a longer time period than originally promised.

If bond issuers just refused to meet their obligations whenever they felt like it then the market wouldn’t work and nobody would lend any money. That puts the onus on heavy borrowers like the UK Government to keep bondholders on side. Being frozen out of the bond market would be a disaster for the country’s ongoing finances.

Equally, while it’s relatively easy to weigh up the chances of your best friend paying you back a tenner, it’s hard to know how much you can trust a government or a corporation with your precious savings.

The role of credit ratings

The bond market uses credit ratings to bridge that gap. Just as you are credit scored for a personal loan, credit rating agencies measure the ability of a bond issuer to make their debt payments.

Low credit ratings equal a high default risk and investors naturally demand higher rates of interest to take that on. Particularly risky bonds are known as high-yield or junk bonds and inhabit the sub-investment grade part of the credit rating scale (see below).

Conversely, bonds with a high credit rating can pay lower rates of interest because they are considered to be of little risk. The quality end of the scale is known as investment grade and starts from the BBB- rating and above.

As with exam results, the real stars get A grades. Any bond rated AA- and over is a minimal risk, high-grade investment. UK government bonds are currently AA-. The top rating is AAA, held by models of financial prudence like Switzerland and Germany.

Minimal risk means a measly interest rate though, so you can’t expect to earn much on high-grade bonds.

Bond investors generally pay attention to the big three credit rating agencies - Moody’s, S&P and Fitch.

Each agency’s ratings system tends to differ slightly but they are broadly comparable. When you assess a

bond ETF, you can find its average credit quality on its factsheet and compare that against an agency’s ratings scale, such as this one by S&P:

| S&P Rating |

Category |

Description |

| AAA |

Investment Grade |

Prime quality. An obligor rated 'AAA' has extremely strong capacity to meet its financial commitments. |

| AA |

Investment Grade |

High grade. An obligor rated 'AA' has very strong capacity to meet its financial commitments. |

| A |

Investment Grade |

Upper medium grade. An obligor rated 'A' has strong capacity to meet its financial commitments but is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions. |

| BBB |

Investment Grade |

Lower medium grade. An obligor rated 'BBB' has adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. |

| BB |

Sub-investment Grade

aka high-yield bonds

aka junk bonds |

Non-investment grade

Speculative, significant speculative characteristics, An obligor rated 'BB' is less vulnerable in the near term than other lower-rated obligors. However, it faces major ongoing uncertainties and exposure to adverse business, financial, or economic conditions which could lead to the obligor's inadequate capacity to meet its financial commitments. |

| B |

Sub-investment grade

aka high-yield bonds

aka junk bonds |

Highly speculative. An obligor rated 'B' is more vulnerable than the obligors rated 'BB', but the obligor currently has the capacity to meet its financial commitments. Adverse business, financial, or economic conditions will likely impair the obligor's capacity or willingness to meet its financial commitments. |

| CCC |

Sub-investment grade

aka high-yield bonds

aka junk bonds |

Substantial risk. An obligor rated 'CCC' is currently vulnerable, and is dependent upon favourable business, financial, and economic conditions to meet its financial commitments. |

| CC |

Sub-investment grade

aka high-yield bonds

aka junk bonds |

Extremely speculative. An obligor rated 'CC' is currently highly vulnerable. The 'CC' rating is used when a default has not yet occurred, but S&P Global Ratings expects default to be a virtual certainty, regardless of the anticipated time to default. |

| D |

Sub-investment grade

aka high-yield bonds

aka junk bonds |

Default. The obligor is unable to pay one or more of his obligations, and S&P does not expect a change of this condition. |

Some providers will also publish a credit quality breakdown of the ETF’s individual holdings on its webpage.

A country’s bonds are rated on a range of factors including:

- The size and sustainability of national debt

- Economic policy

- Economic competitiveness

- Political stability

Corporate bond rating factors include:

- Financial strength e.g. profitability, cashflow, asset valuations

- Competitor threats

- Management skill

- Regulatory and legal environment

- Prospects for the broader economy

Most but not all corporate bonds receive a lower rating than government bonds. After all, companies are generally less likely to survive than countries.

A less obvious distinction is that different bonds from the same issuer can receive different ratings, depending on the terms and conditions of the bond.

Ratings can change too. UK bonds boasted the top AAA rating before the financial crash. But the country’s debt was downgraded in 2013 as our debt burden rose, and we were downgraded again in the wake of the Brexit vote.

Ratings and risk

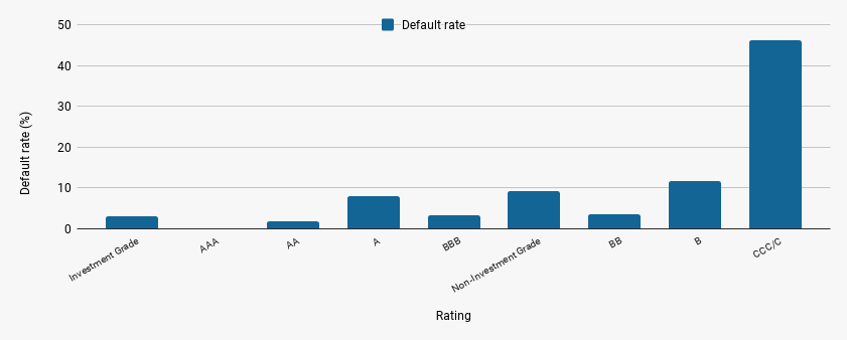

The chart below shows a clear correlation between low government bond ratings and rising default rates. But it also shows that the rating system is not infallible.

Historical default rates since 1993 (time horizon over 12 months)

![Historical default rates since 1993 (time horizon over 12 months)]()

Source: S&P Global Ratings: 2015 Annual Sovereign Default Study And Rating Transitions

Even though AA government bonds are meant to be minimal risk that is not the same as no risk. They can default. The correlation between rating and default rates is also far from perfect as A rated bonds have defaulted more often than BBB since 1993.

Indeed, the rating agencies endured considerable scrutiny after the 2008 financial crisis when default levels rose for some highly rated bonds. It’s worth noting that the rating agencies are paid for their services by bond issuers, which only complicates the difficult task of accurately judging credit risk.

Still the chart shows a clear general pattern. Investment grade bonds are much safer than speculative grade (or sub-investment grade). And the default rate jumps from the CCC level when issuer’s are relying on favourable circumstances to stay upright.

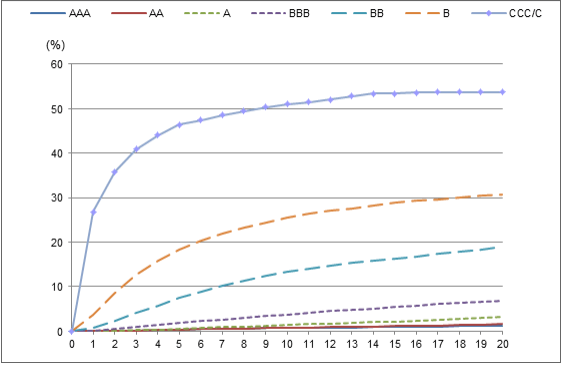

Global Corporate Average Cumulative Default Rates By Rating (1981-2016)

![Global Corporate Average Cumulative Default Rates By Rating (1981-2016)]()

Source: S&P Global Fixed Income Research and S&P CreditPro®

Indeed, this chart shows how investment grade bonds are many times safer than their sub-investment grade equivalents. That’s why you should never take the high yields of junk bond ETFs at face value. Inevitably, default rates will knock back the return you receive, especially during turbulent times when the weak go to the wall.

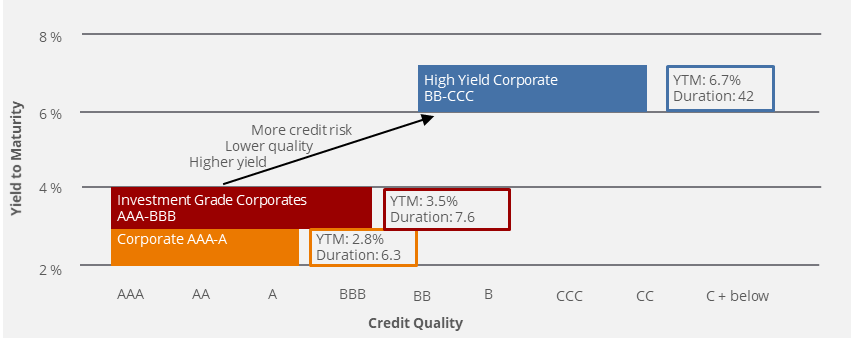

You can actually use the spread in yields offered by equivalent bond issues as a way of judging their relative risk.

Credit Quality Spectrum

![Credit Quality Spectrum]()

Source: BlackRock Blog

For example, as the chart above shows, if a AAA bond yields 2.8%, but a CCC bond of equivalent maturity yields 6.7% then the market is demanding an extra 3.9% to take on the additional credit risk.

The bulk of the minimal risk bond’s yield is compensation for interest rate risk and its maturity date (or term risk). Therefore the extra yield is actually a bonus for taking credit risk. The reward may seem tantalising but you have to accept that it’s only available because you are amping up your credit risk.