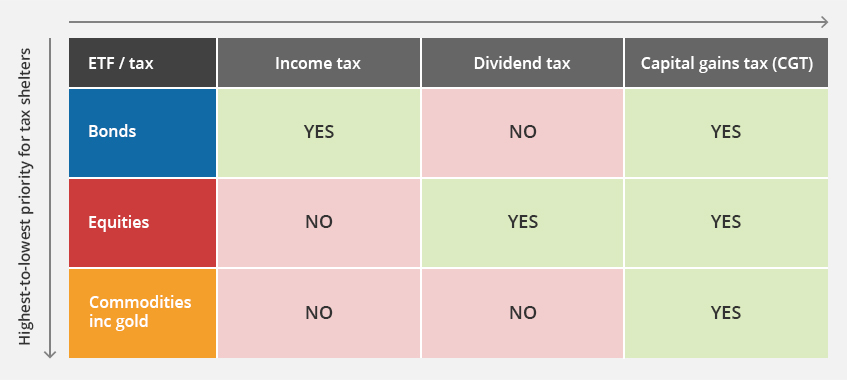

Investments are taxed at different rates in the UK and, though personal circumstances vary, this creates a natural priority order for putting assets into your tax shelters:

Typically, income tax imposes the highest tax rates, followed by dividend tax, while capital gains tax (CGT) is relatively low by comparison. Using this guideline, it’s the most tax-efficient to prioritise bonds in your tax shelters first, followed by equities, while commodities like gold are only subject to CGT.

However, while the general principle is sound, the complexities of the tax system multiplied by personal circumstances mean that there is no simple answer to the question: “What’s the most tax-efficient way to invest in the UK.”

Highest-to-lowest tax rate for typical UK taxpayers

![Highest-to-lowest tax rate for typical UK taxpayers]()

Our tip:

- The same tax treatment applies whether assets are held in funds or as individual securities. The exceptions are individual gilts and qualifying corporate bonds, which are exempt from CGT.

- REIT ETFs are taxed as equities. Direct investments in UK REIT companies are subject to more complicated tax rules that are outside the scope of this article.

- Scottish and Welsh taxpayers pay CGT at UK rates.

- Overseas investments may be subject to withholding tax. This does not apply to ETFs domiciled in Ireland and Luxembourg.

The rest of this article will help you think through your options in the face of this complexity.

justETF tip: Tax exception: The capital gains of off-shore, non-reporting funds are taxed at income tax rates, not at CGT rates. Worse, you can’t offset these capital gains against your annual CGT allowance. Offshore ETFs avoid this fate if they have the UK reporting fund status. The ETF’s provider should state the fund’s reporting status on its website.

You swerve the problem entirely by holding non-reporting funds in your ISAs or SIPPs.

How ETFs are taxed in the UK

Understand how ETFs are taxed to aid tax planning and to ensure you don’t accidentally report the wrong level of taxation on your annual tax return.

More about taxation

Reasons to alter the tax-efficiency priority order

Market conditions

Low interest rates have muted the interest yield and potential capital gains of high-quality, developed world government bonds.

Moreover, bond interest is income tax-free if it falls within your Personal Savings Allowance (PSA).

Therefore you may be able to manage the income tax liability of your bond ETFs via your PSA, saving space within your

ISAs and

SIPPs.

For example, if you’re a basic-rate taxpayer then you’ll pay zero income tax on £100,000 of bonds paying 1% interest per year:

(PSA) £1,000 / 0.01 (1% interest)

= £100,000 worth of bonds that can be sheltered in your PSA before income tax is due.

Higher-rate taxpayers can shelter:

(PSA) £500 / 0.01 (1% interest)

= £50,000 before income tax is payable.

Your holdings are also liable for CGT. The annual CGT allowance for the tax year 2020/21 is £12,300. This is the total amount of profit you can make on all assets subject to capital gains tax during the tax year. If your only unsheltered asset was a bond ETF and it made a capital gain of 10% then:

£12,300 / 0.1 = £123,300 profit is allowed in the tax year before CGT is payable.

If you decide to manage your bond holdings within your tax allowances then it’s a good idea to keep your eye on interest payouts and capital gains if you’re likely to skim close to your thresholds.

Investment objectives

Don’t slavishly follow a general tax-planning rule if it hinders your chance of meeting your objectives.

For example, if you’ve decided that only the higher expected returns of equities will help you hit a university fund target in your child’s JISA, then don’t switch to bonds too soon and jeopardise your objective.

Similarly, the growth potential of equities should be prioritised in a SIPP when your retirement is over a decade away, and you’re in no danger of breaching your Lifetime Allowance.

Bear in mind that placing equities in your ISA/SIPPs for the long-term is more likely to expand your tax-advantaged wealth than prioritising bonds.

Conversely, you’d be right to prioritise short-duration bonds, money market ETFs, or cash over equities in an ISA designed to be a source of emergency funds. Equities are too volatile to function as short-term emergency liquidity.

Heading towards retirement

Higher earners and successful investors may well find themselves taking a tax hit on their pension savings later in life if they breach the Lifetime Allowance.

One way to head this off is to increase your high-quality bond allocation in your SIPPs and reduce your equities, on the assumption that the bonds will grow more slowly.

This move should also lower volatility in your pension portfolio as you glide towards drawdown.

ISAs aren’t burdened by a Lifetime Allowance, nor are they taxed on income like pensions, so you could think about increasing your equity allocation here.

That may help you increase your tax-sheltered wealth while maintaining your overall portfolio asset allocation, as you boost bonds in your SIPPs.

Another useful tip is that your pension wealth is better protected from inheritance tax than your ISAs. However, the inheritance tax rules are complicated and beyond the scope of this article.

Future tax policy

While tax is an inherently unpredictable area, there is considerable debate in the UK about whether CGT rates should be aligned with income tax.

If that happens then it would strengthen the case to prioritise space for equities inside tax shelters given their stronger prospects for capital gains.

You can always rebalance your holdings by selling bonds inside tax shelters and buying equities instead while selling equities inside taxable accounts and buying bonds with those proceeds.

However, if you’ve built up significant capital gains then restrict yourself to selling within your annual CGT allowance as much as possible to minimise your tax bill.

Generally, it’s better to defer paying CGT for as long as possible than to sell up and take the hit.

Your holdings within your tax shelters are not liable for capital gains. You do not even have to report them to HMRC. However, neither can you harvest losses within tax shelters to offset your CGT bill.

Sectors, strategies and sub-asset class types

Certain fund types are more likely than others to incur capital gains, dividends and interest.

For example, tech ETFs tilt heavily towards growth companies that are more likely to reward investors through capital gains than dividends.

Dividend ETFs skew the other way. They’re likely to include a surfeit of strong-dividend payers at the expense of stellar capital gains.

Meanwhile, you wouldn’t expect short-duration, high-quality government bonds to return much in the way of interest or capital gains in the current environment. But high yield bond ETFs necessarily pay higher interest rates to attract investors.

You can see the income-paying history of your ETFs by hitting up its individual web page on justETF.

Go to the Dividends tab, and check out your ETF’s income payouts over the last five years and its current income yield.

justETF tip: Accumulating funds (including ETFs) are still liable for dividend tax, just like

income/distributing funds, if held outside of your tax shelters. You should report your dividends on your self-assessment tax return regardless of whether they were reinvested into the fund or not. The same is true for any

accumulating funds that pay interest. Of course, you may be able to cover your reinvested income using your tax allowances – including your Personal Allowance

However, be careful to deduct your reinvested income from your accumulating fund’s capital gains, or else you’ll unnecessarily pay tax twice. It’s worth mentioning that you should always utilise your tax shelters as much as possible even when you’re just starting out. Capital gains and dividends can grow remarkably quickly, and tax rates and allowances may become less generous in the future.

You can maintain stocks and shares ISA account for the same price as a general investment account with most platforms and, one day, you will be grateful for all the tax paperwork and accountant’s fees you save.

Ultimately, it’s best to tailor your tax-planning to suit your individual circumstances. Although it’s possible to sketch out generic tax efficiency rules for your investments, a balanced approach makes sense in the face of an unknowable future.

The golden rule is always to prioritise your strategic investment objectives first and tax-planning second.