Currency-hedged ETFs are designed to protect investors from

currency risk. They are a simple, cheap and effective way for small investors to access currency management techniques that were once the preserve of major financial institutions.

Currency risk affects you negatively when your home currency strengthens against a foreign currency – reducing the value of your assets held in that foreign currency. That means UK based investors are exposed to currency risk on all non-hedged

ETFs that trade in overseas securities.

Currency-hedged ETFs are useful because they remove the uncertainty of exchange rate fluctuations. They sterilise your portfolio against the effect of currency so that your overseas investment doesn’t gain when the pound falls or lose when the pound rises.

Currency-hedged ETFs: The pros

Global

diversification is near universally accepted as the only free lunch in investing because it offers a route to stronger risk-adjusted returns over time. However, the UK stock market accounts for only 5% of the

MSCI World – leaving a UK investor exposed to currency risk on the remaining 95% of shares tracked by the

index.

While many financial theorists believe that currency volatility is not a major component of long-term equity returns, investors with short time horizons are more vulnerable to exchange rate fluctuations. If you need to tap your portfolio for retirement monies, or to fund some other near-term objective, then you may be forced to sell low when the pound has strengthened – harming your immediate returns. Unlike a long-term investor, you may not be able to wait until an adverse currency move mean reverts. A currency-hedged ETF effectively neutralises this volatility problem.

Currency-hedged ETFs can also be used to express your view on major moves in the currency markets. For example,

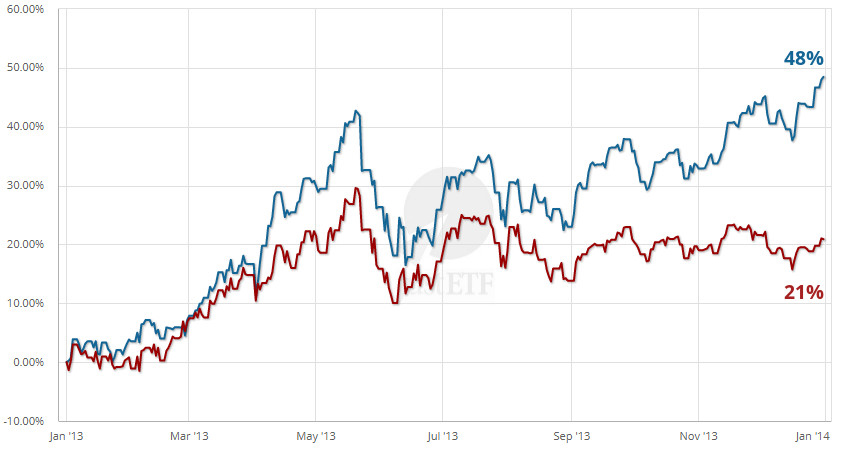

Japan weakened the yen dramatically in 2013 due to the glut of money unleashed by Abenomics. You can see the powerful difference this government policy made to the performance of hedged and unhedged Japanese investments in the chart below:

MSCI Japan ETFs with and without currency hedges (01/01/2013 - 01/01/2014)

![MSCI Japan ETFs with and without currency hedges (01/01/2013 - 01/01/2014)]()

iShares MSCI Japan UCITS ETF (Dist)

iShares MSCI Japan GBP Hedged UCITS ETF (Acc)

Source: justETF Research

As the red line shows, the weaker yen meant that non-Japanese investors saw lower returns on their unhedged Japanese securities between 2013 and 2014 because they were now worthless in pound terms. The hedged ETF performed better (blue line) because the sliding yen was removed from the equation by the currency hedge.

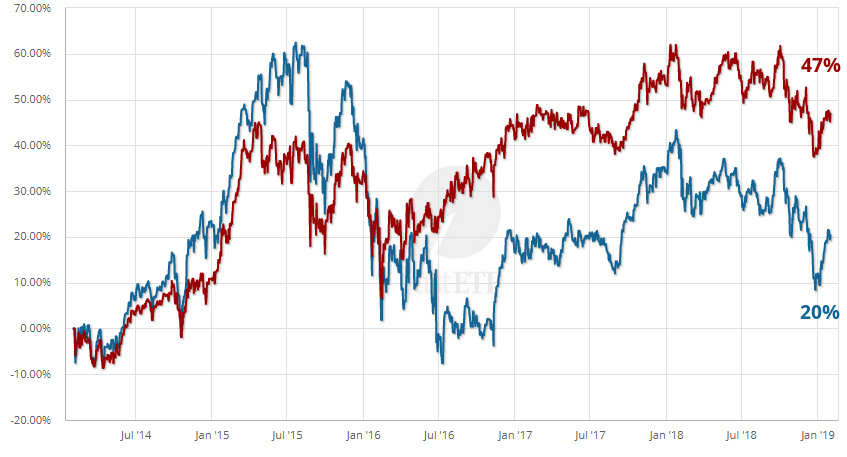

MSCI Japan ETFs with and without currency hedges (31/01/2014 - 31/01/2019)

![MSCI Japan ETFs with and without currency hedges (31/01/2014 - 31/01/2019)]()

iShares MSCI Japan UCITS ETF (Dist)

iShares MSCI Japan GBP Hedged UCITS ETF (Acc)

Source: justETF Research

Yet the unhedged ETF bounced back and performed more strongly over the next five years as Abenomics ran out of steam. An investor who believed that the weakened yen of 2013 would rise again when the quantitative easing taps were turned off, could have positioned their portfolio to profit from this expectation.

Of course, this is easy to say in hindsight and the reality is that currency moves are hard to anticipate. To take a topical example that’s close to home: most UK investors can’t help but wonder how they should deal with Brexit. It’s natural to believe that a no-deal scenario would weaken the pound further – improving the returns of unhedged overseas ETFs. Whereas a better-than-expected deal could favour hedged overseas ETFs whose value would be protected against a rising pound. Which way will it go? There isn’t a crystal ball on Earth that can tell us, although very few UK investors predicted that their global portfolios would benefit from the “No” vote in 2016.

Currency Hedged ETFs: How do they work?

Currency-hedged ETFs and non-currency-hedged ETFs use the same asset allocation (assuming they’re issued by the same provider and track the same index – as many do). The important difference is that currency-hedged ETFs typically use forward exchange contracts to hedge against exchange rate fluctuations.

The value of the forward exchange contracts corresponds to the value of the ETF’s assets. If your home currency strengthens (reducing the value of your overseas investments), then the forward contracts should gain enough to offset your losses. If your home currency weakens then the forward contracts are liable to lose enough to wipe any currency gain.

Hence, currency fluctuations cancel out either way and you experience approximately the

return of the local equity market. Why only approximately? Because no currency hedge is perfect. Inevitably there will be a slight mismatch between the estimated value of the ETF covered by the hedge and the ETF’s actual market value. For example, if the forward contract was designed to cover $10 million but the ETF rose in value to $12 million, then a portion of the securities are no longer fully hedged. Currency hedging involves some timing risk too. For example, if the forward contracts expire on a monthly basis then the hedge will be less accurate than if contracts are taken out on a daily basis. The tradeoff is that daily hedging is more expensive and those higher costs can erode returns.

The main costs of currency hedging include:

- The spread incurred when pairs of currencies are traded (essentially the same as a bureau de change charging you for converting pounds into foreign currency).

- Transaction costs

- Holding costs

The cost of holding a currency – also known as the ‘cost of carry’ – is determined by the interest rate differential between a pair of currencies e.g. the pound and the dollar. The cost of carry is positive when the pound’s interest rate is the higher of the two. The cost of carry is negative when the pound’s interest rate is lower than its foreign currency partner.

An efficient hedge requires liquid derivatives and favourable trading conditions, so hedging is generally only worthwhile for the major world currencies. The high interest rates and wide spreads of emerging market currencies mean there are few currency-hedged ETFs available in this space.

ETF providers often recover their currency hedge costs through a slightly higher Total Expense Ratio ETF (

TER). Many currency-hedged ETFs are 0.1% to 0.3% more expensive per year than their unhedged counterparts. However, you will occasionally find no cost differential at all.

Hedged ETFs: How to find the right currency-hedged ETFs

There’s a range of currency-hedged ETFs that cover the major equity markets, global bonds, gold and broad commodities (in the latter two cases you’re exposed to the dollar). And you are well served whether your home currency is the pound, euro, dollar, yen or Swiss franc. You should choose ETFs that hedge the currencies in which you expect to pay your bills. Therefore most UK-based investors will want "GBP hedged" ETFs. Look out for that term in the

ETF’s name and double check the ETF’s factsheet or webpage to confirm its GBP hedged status.

Find the best currency-hedged ETFs

Use the ‘GBP hedged’ filter function in our ETF search to easily find UK appropriate currency-hedged ETFs.

To the ETF Search

Good to know: Currency-hedged ETFs are usually issued as a separate share class of an existing ETF. That keeps costs low and means the ETF doesn’t

have to scale much to be sustainable. Fund volumes are often small but you can find more information about that on the ETF’s factsheet.

You can use the tracking difference between the currency-hedged ETF and its corresponding index to see how accurate the hedge was and how much it cost you beyond the TER. You can use our comparison function to assess this – although it’s only worth drawing conclusions when there are at least three years of data available.

ETFs with and without currency hedging in pounds for selected indices

| Index |

Country/Region |

Number

of ETFs |

Fundsize

in m GBP |

2026

in % |

| EURO STOXX® 50 |

Europe |

11 |

28,961 |

9.96% |

| EURO STOXX® 50 (GBP Hedged) |

Europe |

2 |

353 |

12.43% |

| JPX-Nikkei 400 |

Japan |

2 |

175 |

17.06% |

| JPX-Nikkei 400 (GBP Hedged) |

Japan |

1 |

9 |

20.66% |

| MSCI Australia |

Australia |

3 |

748 |

9.71% |

| MSCI Australia (GBP Hedged) |

Australia |

1 |

4 |

8.96% |

| MSCI Canada |

Canada |

4 |

3,388 |

8.24% |

| MSCI Canada (GBP Hedged) |

Canada |

1 |

211 |

11.52% |

| MSCI EMU |

Europe |

5 |

9,463 |

11.41% |

| MSCI EMU (GBP Hedged) |

Europe |

4 |

353 |

13.96% |

| MSCI Europe ex UK |

Europe |

2 |

1,310 |

10.00% |

| MSCI Europe ex UK (GBP Hedged) |

Europe |

1 |

180 |

12.61% |

| MSCI Japan |

Japan |

12 |

20,624 |

17.00% |

| MSCI Japan (GBP Hedged) |

Japan |

3 |

404 |

23.35% |

| MSCI Switzerland 20/35 (GBP Hedged) |

Switzerland |

2 |

112 |

12.04% |

| MSCI USA |

United States |

14 |

37,343 |

11.22% |

| MSCI USA (GBP Hedged) |

United States |

2 |

36 |

9.15% |

| MSCI World |

World |

18 |

215,819 |

11.07% |

| MSCI World (GBP Hedged) |

World |

7 |

2,243 |

8.37% |

| S&P 500® |

United States |

24 |

313,075 |

11.37% |

| S&P 500® (GBP Hedged) |

United States |

9 |

6,677 |

10.14% |

Source: justETF Research; as of 30/06/2026; all calculations in GBP