Bonds have been on a bad run despite their reputation for stability. This article explains why bonds don’t always work, why they’re still useful, and how the short-term pain translates into long-term gain.

Unquestionably, we’re experiencing the toughest period for bonds in decades. The reason is straightforward: nominal bonds take a hit when inflation is unexpectedly high. Every asset class has its Kryptonite. And just as equities dip during a recession, bonds run into difficulties when central banks lose their grip on inflation.

Stay up to date

Free English newsletter including the latest news & knowledge about investing in ETFs.

Firstly, governments are serious about taming inflation.

Secondly, the hardship bonds are dealing with right now is a form of growing pain. When the turmoil subsides, bonds will be more profitable than before.

Here’s how it works ...

Short-term pain

Rising inflation eats away the interest investors earn from their bonds. Investors naturally respond by demanding a higher interest rate. But older bonds are like fixed rate savings. They’re stuck with their original coupon rate until they mature.

This is a problem because why would you hold a bond earning 2% interest when new bonds earn 3%? Bond traders solve the problem by selling their less competitive bonds at a discount.The process is like a shop slapping on ‘Sale’ price stickers to clear older goods. This discount price makes each old bond worth exactly the same as its new bond equivalent.

An example

Imagine you’re offered two identical bonds that pay back 100€ in 12-months plus a fixed coupon rate in the meantime. (The coupon is the amount of interest a bond pays on its principal – see our bond explainer).

The first bond pays 3% interest and is priced at 100€.

The second, older bond only pays 2% interest. Its market price will be 99,03€. That lower price means the older bond is now as profitable as the first bond. The discount means both bonds yield a 3% return if you hold them until they mature.

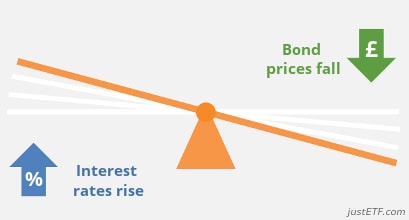

This mechanism explains why existing bonds lose value when interest rates rise. The rise forces the market to reprice bonds with lower coupon rates to make them competitive against new, higher yielding bonds entering the market.

When market interest rates rise, bond prices fall. When interest rates fall, prices rise.

When interest rates rise, the mechanism is equivalent to last year’s iPhone dropping in price when the latest version comes out. Last year’s iPhone still works. It just isn’t as shiny as this year’s model.

(Unlike iPhones, market interest rates can fall back again. In this instance, new bonds come on to the market with lower coupons than their older peers. Hence the price of older bonds rises because they offer more interest and people will pay more for that.)

OK, so that explains how we got here. To recap:

Rising inflation triggered rising interest rates. That caused our bond ETFs to fall in value as their older bonds were marked down in price.

This is the short-term pain. Now for the long-term gain.

Long-term gain

As the older bonds near maturity they’re sold off and replaced with higher yielding versions. Those higher-yielders pay more income than before. Eventually those stronger cashflows completely erase earlier capital losses. And ultimately, you’ll earn better returns than if interest rates hadn’t shot up.

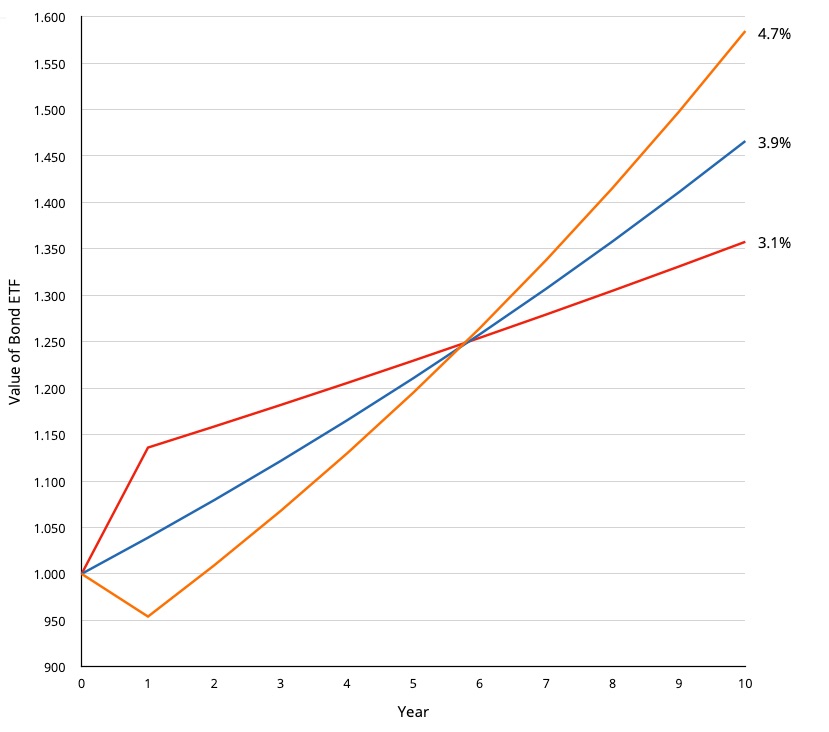

This rising yield scenario shows you how the maths work:

Interest rate effects on an hypothetical bond ETF for 10 years

Rising yield Static yield Falling yield

Source: justETF Research, interest rate effects on hypothetical bond ETF. Interest reinvested. 0% costs.

Rising yield scenario: The orange line shows you the fate of a bond ETF worth 1,000€ after an initial 2% rise in interest rates. Rates remain flat after the rise.

Static yield scenario: The blue line represents the ETF’s growth if interest rates had stayed the same.

Falling yield scenario: The red line shows you the bond ETF’s growth trajectory over ten years, if interest rates had initially dropped 2% instead of rising. Rates remain flat after the drop.

As you can see, the rising yield scenario is the most profitable over ten years. The orange bond ETF must deal with initial losses but then overtakes the blue and red growth lines after five years. It’s well ahead after a decade of earning higher income.

Much as the initial losses hurt, they set the stage for later gain. The rising rate scenario proves to be the best of the three alternative timelines.

The long-term effect of rising rates is that – after they flatten out – you’re in a better position than before. It’s like weight training at the gym. It’s tough at the time but eventually the hard work pays off. In this case, you’re rewarded with a pumped-up bond position.

Any caveats?

It works faster with shorter maturity bonds ETFs. Long bond ETFs are slower to recover because their older bonds take a bigger initial hit, and then hang around for ages before they disappear.

The long bond reward may well be greater in the end, but it’s better to match your bond ETF’s duration to your investment time horizon, than to think purely in terms of profit.

But the size and speed of the effect varies depending on your holdings’ specific properties such as average coupon, yield-to-maturity, duration, average maturity, credit risk, cost, and so on.

Results are also dependent on the future path of market interest rates.

The scenario above is necessarily simplified. In reality, interest rates fluctuate every day.

If interest rates rose gently then you may well barely notice your ETF’s loss. We’re feeling the pain at the moment because the rises have been steep as the world rapidly adjusts to the threat of inflation.

The rising yield scenario also works better if:

You reinvest interest. Choose an accumulation ETF to set that on auto-pilot.

You cost-average new money into your bond ETF. That hastens the speed at which you buy better value bonds.

You’ll also get a capital gains boost if market interest rates fall back. That offers a nice sugar high, though as we can see above, lower interest rates ultimately make our bond ETFs less profitable. Which is why rising yields are ultimately a good thing.

Global ETF investment

Discover the best ETFs on the MSCI World Index in our investment guide!

Provide you with reserves to rebalance into equities when they go on sale.

High-quality, investment-grade government bonds are particularly good in that role and that hasn’t changed.

The question is: do you think a recession is less likely or more likely at the moment? If you’re worried about an economic downturn, then it’s a sound idea to hold government bonds because they’re usually the best performing asset class in that scenario.

Government bonds provide portfolio defence

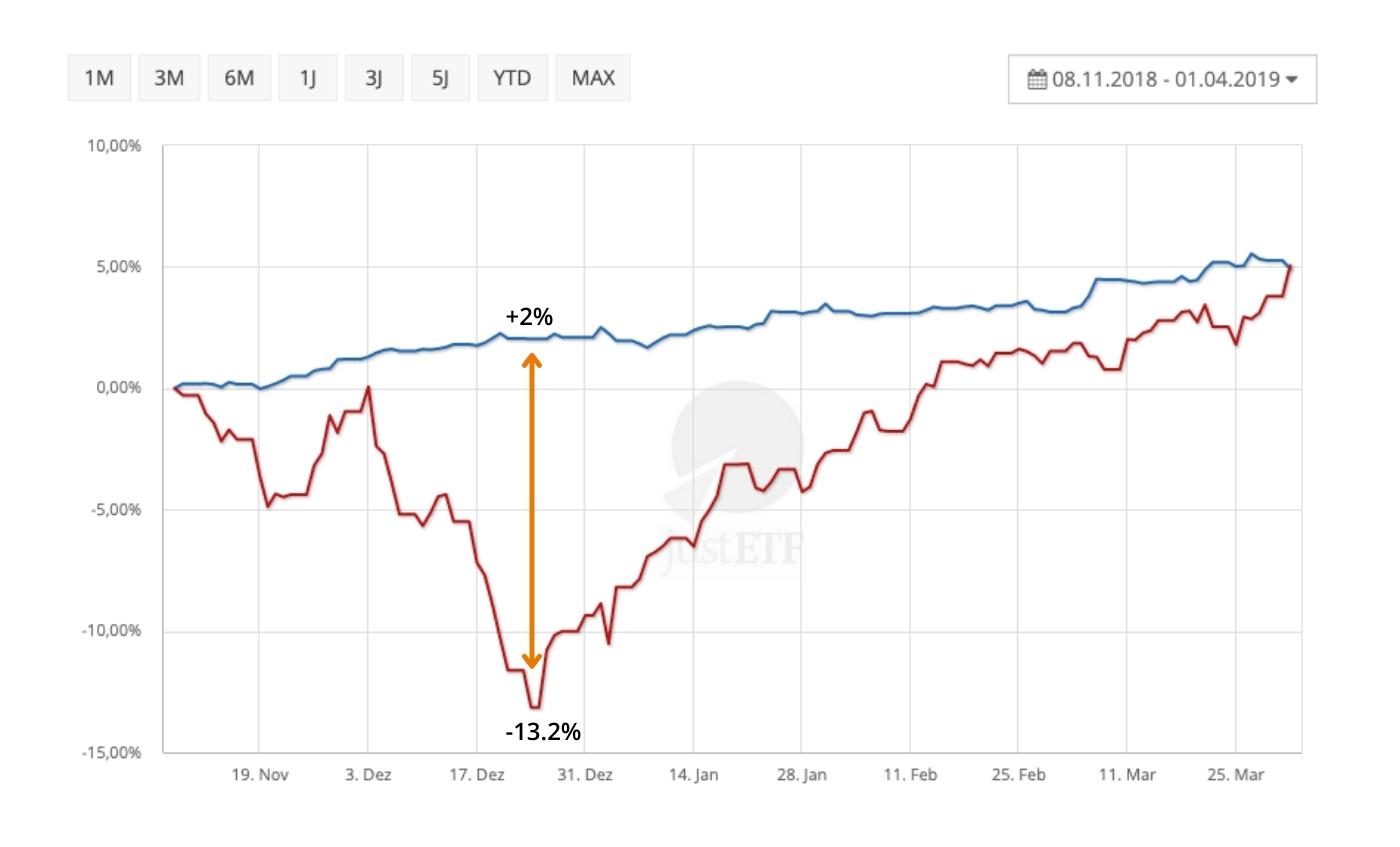

Let’s see how high-quality government bonds performed in difficult conditions going back to the Global Financial Crisis. In each case, we’ll compare an intermediate, high-quality, government bond ETF against a MSCI World equities ETF.

The blue line shows the bond return, equities are in red, and the orange arrows show the performance differential at the point of maximum crisis:

The Covid Crash

iShares Euro Government Bond 7-10yr UCITS EUR (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research; 18.10.2022

Government bond returns were slightly negative but they were still a sight better than equities. Happily, the world’s major Central Banks soon rode to the rescue.

2018 Global Stock Market Downturn

iShares Euro Government Bond 7-10yr UCITS EUR (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research; 18.10.2022

Christmas 2018 delivered a lump of coal to all equity investors while government bonds proved to be a better present.

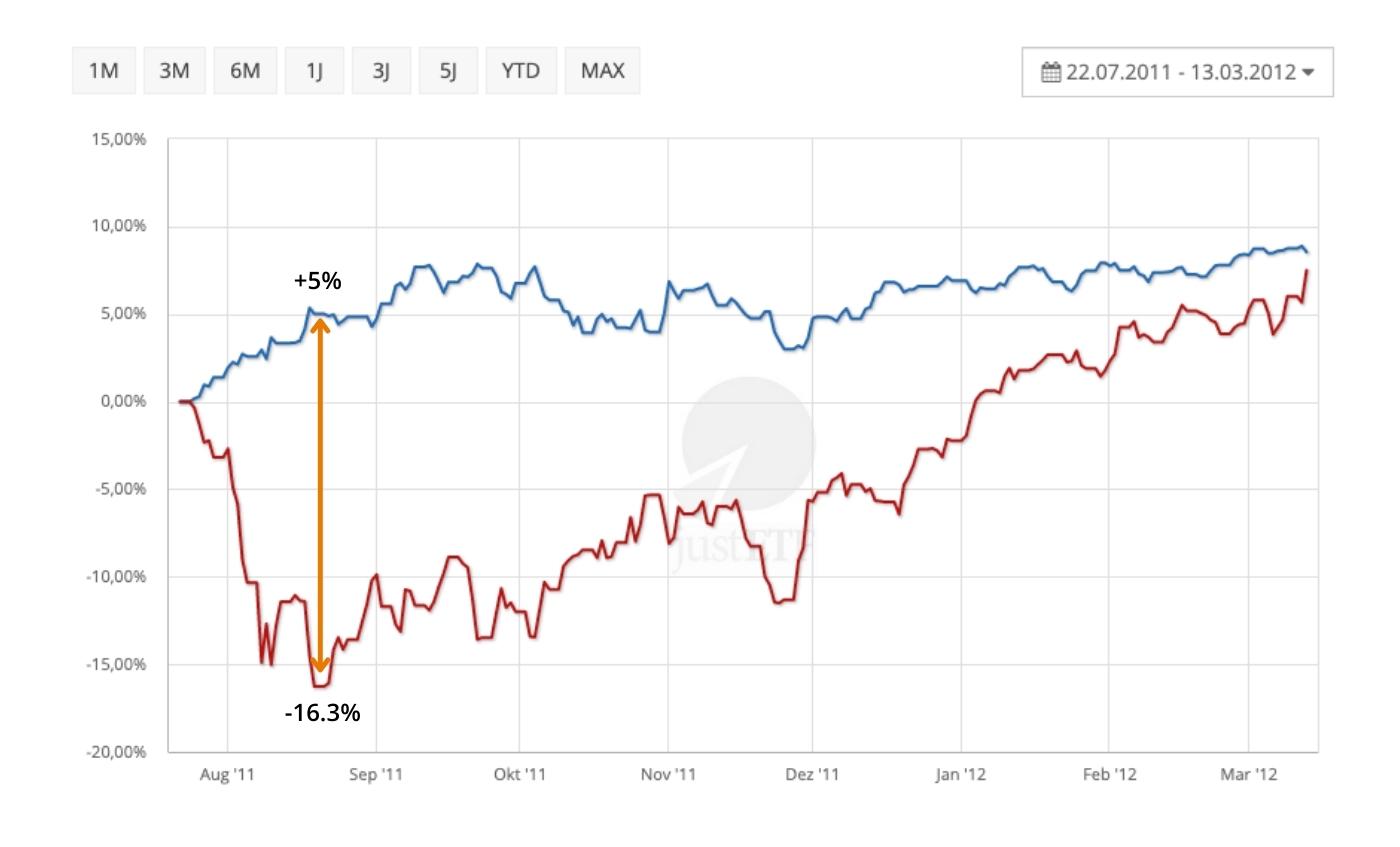

August 2011 Stock Market Downturn

iShares Euro Government Bond 7-10yr UCITS EUR (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research; 18.10.2022

Once again government bonds were a positive counterweight to plunging equities. If you rebalanced from government bonds into cheaper equities at this moment you’d have booked a nice profit.

iShares Euro Government Bond 7-10yr UCITS EUR (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research; 18.10.2022

Investors were rattled about European debt yet our European government bond ETF held up through multiple equity market sell-offs.

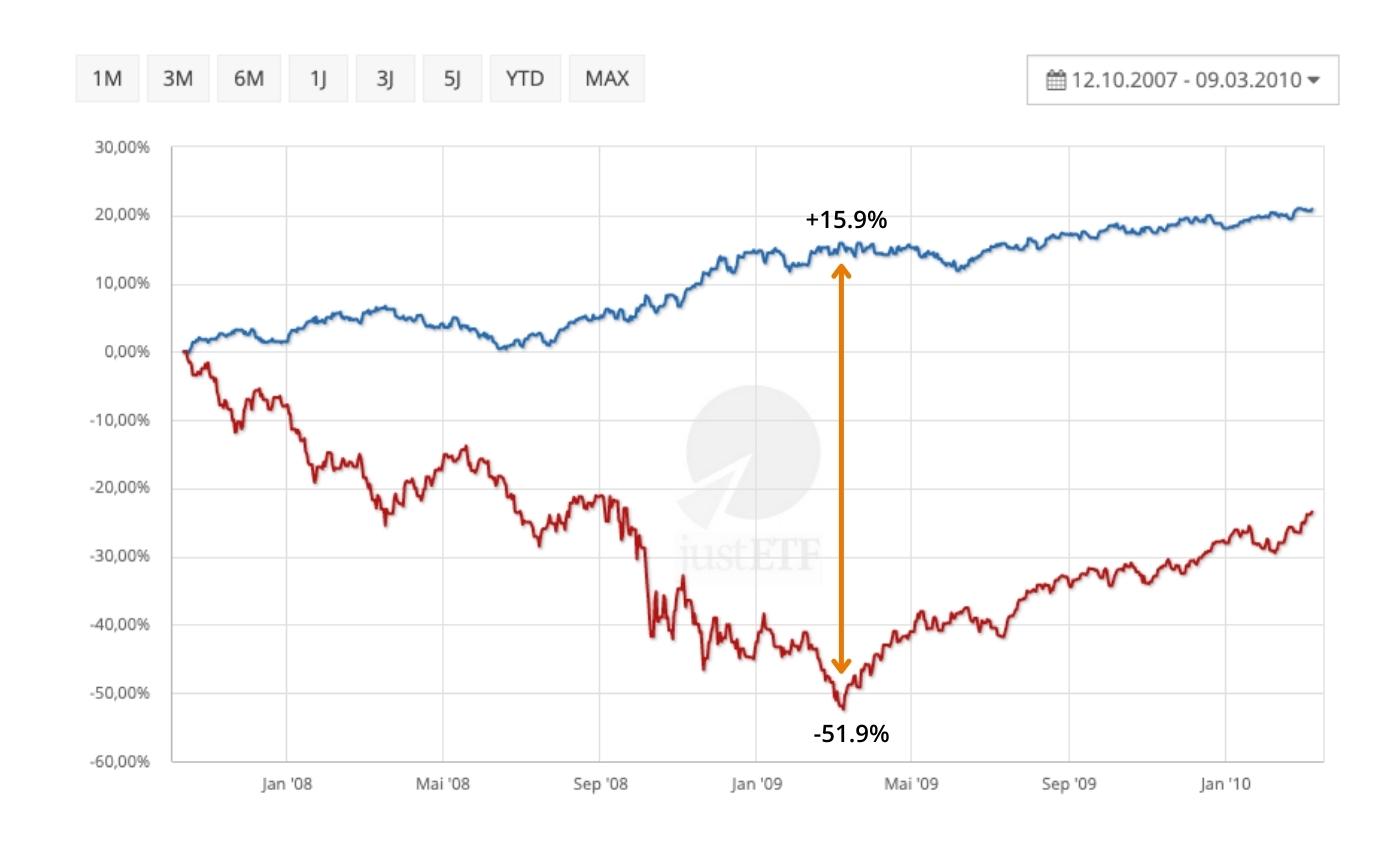

Global Financial Crisis

iShares Euro Government Bond 7-10yr UCITS EUR (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research; 18.10.2022

This is the big one. Equities shed an eye-watering 52% but government bonds proved to be a safe haven during the storm.

The Global Financial Crisis is the textbook example of why every investor should maintain an allocation to government bonds.

When investors panic they often flee into government bonds. If you already own this asset class then there’s a strong chance its value will spike just when you need it most.

Government bonds also proved a strong counterbalance to tumbling equities during the other big crash of the 21st Century: the Dotcom Bust. Sadly there weren’t any European government bond ETFs around at the time to make diversification as easy as it is now.

Of course, investing doesn’t operate like clockwork. There certainly have been occasions in the past when bonds haven’t been the answer.

Our conclusion

Conventional bonds don’t work well when inflation runs riot and rising interest rates could still dish out more pain. But the best way to increase your long-term expected bond returns is to keep investing at higher yields.

And when recession strikes and demand slumps, bonds are usually your best defence.

Stay up to date

Free English newsletter including the latest news & knowledge about investing in ETFs.