ETFs let you own the world. Within the space of a few funds, you can invest in every major country and publicly traded asset class - enabling you to harness the power of

diversification, juice your returns and reduce volatility. What’s less well understood is that overseas investing exposes you to currency risk. It makes no difference whether you use ETFs or direct investments. The most beautiful increase in value or dividend strategy is of little use if an unfavourable exchange rate cancels out the return or even drags it into negative territory. There are indeed insurances against exchange rate fluctuations, so-called

currency-hedged ETFs. But first, you should assess how much of your own investment actually depends on the development of foreign currencies.

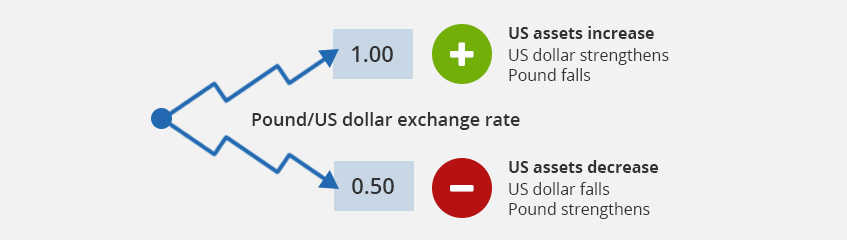

What exactly is currency risk? Currency risk is the impact of exchange rates upon your overseas investments. Let’s say you own US equities and the US dollar weakens against the pound by 5%, but US stock market prices don’t actually change. The result is:

- Your US equities fall by 5% when their value is converted into pounds - the currency you pay your bills in as a UK resident.

Currency risk can work in your favour too. If the dollar strengthens by 5% against the pound (the US stock market is again unmoved) then:

- Your US equities rise by 5% when their value is converted into pounds.

In both these scenarios, a US resident investor wouldn’t see anything to get excited about. Their return is 0% over the period. But a UK investor either gains or loses 5% based purely on the fluctuation of the dollar: pound exchange rate. That’s currency risk.

Exchange rates create opportunities and risks for ETF investors

![Exchange rates create opportunities and risks for ETF investors]()

Source: justETF Research

Exchange rate fluctuations also add to and subtract from the local returns of overseas securities. For example, if US stock market prices dropped 5% while the dollar simultaneously lost 5% against the pound, then a UK investor would see a 10% total loss (-5% local return plus -5% dollar: pound return).

If the US stock market had increased 5%, then a UK investor would register a 0% return - the local gain is wiped out by the adverse exchange rate move.

Again, this works in reverse. If the dollar strengthened 5% in tandem with a US stock market 5% rise, then a UK investor would gratefully accept a 10% total return. If the US market lost 5%, then the strengthening dollar compensates the UK investor for the loss, and they end up with a 0% return. Meanwhile, a US investor would be sitting on a 5% loss.

The same goes for any security that’s priced in a foreign currency. Your returns equal the change in the local value of the security, plus or minus the change in the exchange rate.

Currency risk can make a big impact in the short term. An overseas market can make decent annual returns that are nullified by a strengthening pound. Or a weakening pound can supercharge your overseas assets - as happened in 2016 when the pound sank 20% against the dollar. The returns of certain strategies can be entirely drowned out by the volatility of exchange rates, think Emerging Market bonds denominated in local currencies.

Currency risk of ETFs: Should you fear it?

Your time horizon matters. Your vulnerability to exchange rate volatility increases if you need to sell your investments in the short run. Exchange rate fluctuations can be violent - as the Brexit vote aftermath has shown. Volatility is particularly dangerous for forced sellers who can’t just ride it out, so you may well want to protect your portfolio from currency risk if you must regularly draw down from it.

Longer-term investors have much less to worry about and may even benefit from currency risk. Studies show that exchange rate fluctuations make little impact on equity returns as time horizons lengthen. Economists who advocate Purchasing Power Parity between countries believe that currencies reach equilibrium over time, and therefore exchange rate fluctuations tend to net out. Many commentators believe that there’s no expected return from taking currency risk, but that it can reduce the volatility of your holdings by reducing the correlation of returns between overseas assets held in different currencies. In other words, global equities will naturally tend to hedge each other as rising currencies are offset by falling ones.

It’s important to distinguish between equities and government bonds, however. The intrinsic volatility of equities means that exchange rate fluctuations are less relevant to your long term returns. However, currency risk can have an outsized impact on low volatility global bonds. Therefore, it makes sense for investors to hedge currency risk out of their bond allocation when you want that part of your portfolio to play its traditional role in dampening volatility.

What’s your currency risk exposure?

Before we look at your currency risk options, it’s a good idea to estimate your portfolio’s overall currency risk first.

The

MSCI World index illustrates how you can work this out. The index tracks the stock markets of 23 industrialised countries, as you can see in the diagram below. It’s dominated by the US. About two-thirds of an MSCI World ETF is invested in US equities, and those assets are priced in US dollars. In other words, a UK based investor’s MSCI World ETF holding is 60% exposed to the pound: US dollar exchange rate. Equities priced in pounds make up 5.8% of the index, so your overall currency risk is 94%. As you can see, 8% of the currency risk is against the yen, while there’s 0.3% exposure to the Norwegian krone.

Currency weightings - MSCI World ETF

U.S. Dollar (USD)

Euro (EUR)

Japanese Yen (JPY)

British Pounds (GBP)

Canadian Dollar (CAD)

Swiss Franc (CHF)

Australien Dollar (AUD)

Hongkong Dollar (HKD)

Swedish Krone (SEK)

Danish Krone (DKK)

Singapore Dollar (SGD)

Norway Krone (NOK)

New Shekel (NIS)

New Zealand Dollar (NZD) |

66,6%

10,1%

6,9%

4,3%

3,4%

2,9%

2,2%

1,2%

0,9%

0,8%

0,3%

0,2%

0,1%

0,1% |

Source: iShares Core MSCI World UCITS ETF; as of 09/06/2021

Obviously, a UK investor is taking more currency risk than a US investor if they’re both invested 100% in the world portfolio.

ETF currency risk: your options

Currency risk doesn’t have to be a binary choice. There’s a number of ways that you can manage your exposure:

- Avoid: Increase your asset allocation to your own currency area, i.e. invest in UK equities, property and bonds if you settle your bills in pounds. The obvious downside is that you’ll be less diversified, especially as the FTSE 100 and FTSE All-Share are heavily skewed to three sectors: financials, energy and consumer staples. Both indices are also dominated by global large caps like HSBC and Royal Dutch Shell that earn most of their revenue abroad. Around 75% of FTSE 100 firms’ earnings come from overseas, which means that they too are heavily exposed to currency risk. When the pound falls, those foreign earnings are worth more in pounds, boost the share price of the major players in the index, and boost your FTSE 100 or FTSE All-Share ETF. Again, the same is true in reverse and also true for the dividends you receive. If you want to engineer more home bias in your portfolio, then the firms tracked by FTSE 250 ETFs are much more reliant on UK based earnings.

- Currency-hedged ETFs: These products are a very cheap and straightforward way to neutralise currency risk. Currency-hedged ETFs use financial contracts to offset the effects of exchange rates on fund returns. The hedge is a form of insurance that cancels out the loss you experience from a falling overseas currency. Sadly, the contract also cancels any win you experience from rising overseas currencies too. You can’t have it all. The currency hedge means you experience approximately the same return as a local investor (hedges aren’t always perfect) and currency risk is largely removed from the equation. Read more about the pros and cons in our article on currency-hedged ETFs.

- Diversify: Splitting your assets between different assets and markets reduces your investment risk. The same applies to foreign currencies, as discussed above. Intriguingly, you can also benefit from your exposure to safe-haven currencies like the dollar and euro. The dollar especially has exhibited a negative correlation with world equity prices historically. Because the dollar is the world’s reserve currency and is used as a store of value by corporations and ultra-high-net-worth individuals, its rising value can cushion the blow of falling equities for a non-US investor. Your risk also changes if you split your residence between different currency areas. If you live in the UK for part of the year and France, say, for the rest of the year (or think you will) then you should hold assets in pounds and euros, so you can pay your bills in both countries without concern for currency risk. Diversification is also the answer if you fear the long-term decline of the pound - overseas assets are an ideal hedge against that scenario.

- Long-term investment: Financial theory and evidence indicates that stock market returns are driven by a country’s economic performance over the long term. Therefore, our ETF portfolios offer long-term investment strategies that enable you to harness GDP growth opportunities across the entire world as opposed to the futile task of trying to predict short-term market fluctuations.

- Partial hedging: You can, of course, hedge out some currency risk but maintain enough to enjoy some benefit from currency diversification. The customary strategy for a long-term investor is to allow currency risk on the equity side of your allocation while hedging on the bond side, or investing purely in UK government bonds.

ETF currencies: cutting through the confusion

Many people are exposed to currency risk without realising it because there’s a profusion of confusion when it comes to the currency labels applied for funds. Let’s clear that up:

1. Underlying currency

Have you ever seen a World ETF that says its currency is dollars, while another version of the same product is labelled in pounds? That makes no difference whatsoever to your currency risk. What counts is your exposure to the currency of the underlying securities trade-in. Returning to our MSCI World pie chart from earlier, 60% of your currency exposure is to the US dollar because 60% of the ETF’s securities are traded in that currency on the US market. 8% of your exposure is to the yen, and so on. This has two important implications. If a World ETF is labelled in US dollars (see the other terms below to understand why that happens), your currency exposure to the US dollar is still only 60%. Your 8% Yen risk isn’t somehow amplified by dollar risk too. A UK investor in Japanese securities is only concerned with the yen: pound exchange rate. The dollar isn’t part of that equation. An ETF labelled in pounds doesn’t save you from currency risk either unless it's specifically GBP hedged (more on that below). Therefore, to understand your currency risk, you need to know which currencies an ETF’s underlying securities are traded/priced in.

justETF tip: ETF providers typically state the product’s asset allocation by country in its factsheet and webpage. This will give you a rough and ready reckoning of your currency risk exposure. You can usually find the link to the factsheet from the ETF profile at justETF.

2. Fund currency

This term is responsible for much of the confusion surrounding ETF currencies. The terms base currency or denominated currency are also often used. Crucially, these terms refer to the currency that an ETF reports in, not necessarily the currencies that the underlying securities trade-in. The ETF reports its Net Asset Value in the fund currency and distributes income in that currency too. Your broker will convert your income into pounds, but will likely charge you an exchange rate fee for doing so. The fund currency is generally based on the currency used for the underlying index. The index currency is usually the same as the currency in which most of the

index’s securities are traded.

justETF tip: The fund currency is displayed on each ETF profile at justETF.

3. Trading currency

The trading currency means the currency in which the ETF itself is bought and sold on a particular exchange. The units/shares of a World ETF may be traded in pounds because it’s listed on the London Stock Exchange (LSE) but that doesn’t alter the fact that you’re exposed to the currency risk of its underlying securities. Intriguingly, the LSE allows trading in multiple currencies, so it’s worth making sure you invest in a pound version where available to avoid more exchange rate conversion fees.

justETF tip: Use the Exchange tab on the ETF profiles at justETF to reveal the trading currency of your ETFs.

4. Currency hedging

You should choose GBP-hedged ETFs if you’re a UK resident investor who wants to eliminate currency risk as much as possible. Appropriate ETFs will normally have the term ‘GBP Hedged’ in their names, but always check the product’s factsheet or webpage to make sure. If you can’t find any reference to GBP hedging in the ETF’s name or literature, assume it isn’t hedged. You’ll also notice that hedged ETFs are often a little more expensive than their unhedged counterparts. That’s because the hedge itself incurs costs.

justETF tip: You can easily find GBP hedged ETFs by using our

ETF search.

Why do exchange rates fluctuate?

Exchange rates mainly result from the forces of supply and demand for national currencies. For example, the currency of a leading export nation is likely to strengthen over time because of the high demand for its goods, all things being equal. The currency markets also influence exchange rates. Currency traders move swiftly to exploit any arbitrage opportunities. The carry trade is a famous example - traders borrow in a low-interest rate currency and buy into a high-interest rate currency. The aim is to profit from the interest rate differential. However, arbitrage opportunities are usually fleeting and high risk, as exchange rates move to reset the market equilibrium between pairs of currencies.

Naturally, central banks influence the value of their national currency through monetary policy. You can see this playing out as countries recover from the Global Financial Crisis at different rates. The US-led the Developed economies out of the crisis and has been able to raise interest rates faster than the Bank of England or the European Central Bank. Hence, the US dollar has strengthened against the pound in recent years, benefitting UK investors who held significant US assets. Other countries are known for playing a more active role in their exchange rate.

China, for example, is thought to manage the rise of the Yuan to preserve the competitiveness of its export sector.

Some countries may peg the value of their currency to a stronger currency, in which case there’s no currency risk as long as the peg sticks. Many Emerging Market economies also find it easier to raise finance if they issue their bonds in US dollars. This can lead to major economic turmoil if a country’s debt burden soars because its currency then falls against the dollar and overseas earnings don’t compensate. Argentina is the cautionary tale par excellence here.

The main takeaway is to recognise that the currency markets are among the most efficient and competitive in the world. Small investors have neither the speed nor information to prosper for long in this space. Therefore, it’s best to adopt a currency risk position on a strategic level that aligns with your long-term goals.