Choosing a bond ETF is the number one way to diversify your portfolio after you’ve bagged a global equities ETF. Bonds play defence while equities play offence. Bonds offer stability while equities offer growth. For these reasons, owning a bond ETF is key to bringing balance to your portfolio.

But the bond market is huge and confusing. Not all bonds help us manage our risks. So we’ve written this guide to enable you to rapidly identify your ideal defensive partner from the vast range of bond ETFs out there.

Step one is to focus our selection on the bond ETFs that best protect us against stock risk. Afterall, most people’s portfolios are dominated by equities. So our most important diversification move is to hold the defensive assets that are most likely to perform when the stock market is in retreat.

And those assets are high-quality government bonds.

High-quality means developed world government bonds that are rated investment grade and above. These bonds are the least risky type because they’re backed by the economic strength of strong and stable countries that are extremely unlikely to default on their national debt.

Investors often flock to the comparative safety of government bonds during a recession because countries are much less vulnerable than companies during times of crisis.

The surge in demand for government bonds pushes up their price, and cushions the impact of equity losses on your portfolio. This “flight-to-quality” effect isn’t guaranteed everytime but it often works. It’s the main reason why high-quality government bonds are good diversifiers of equity risk and are the core defensive asset class used in ETF portfolios.

Which high-quality government bond ETF?

A European investor should choose a Euro government bond ETF. A Euro government bond ETF holds a range of fixed income securities diversified across Eurozone countries.

Why is it important to choose a Euro denominated fund? Because bonds that are not valued in your home currency expose you to currency risk. That adds unwelcome volatility to the defensive part of your portfolio. We want our bonds to improve portfolio stability so it’s best to eliminate currency risk from that side of the equation.

justETF tip: There are some currency hedged global government bond options that work, too. We’ll cover those products below but they’re not a necessary addition as Eurozone ETFs are already well diversified.

We can safely ignore other types of bonds because they are typically not as good at diversifying equity risk as government bonds. So junk bonds, corporate bonds, emerging market bonds and the rest can all be crossed off our list.

Inflation-linked bonds are a good option for a second bond ETF but we’ll come back to those. For now, let’s stay focused!

Choosing the right bond ETF maturity

Our next most important decision is to choose our bond ETF’s maturity. An individual bond’s maturity date works like a fixed rate savings account. If a savings account (or bond) has a maturity of three years then, at the end of that time, the issuer pays back the original amount of money loaned (also known as principal). In the meantime, the bondholder is paid interest as compensation for the risk they bear.

Long loans are riskier than short ones which is why the bank pays more interest when you lock up your money for five years instead of one.

The same is true for bonds. This fact of life leads to a helpful rule-of-thumb: longer maturity bonds are riskier than shorter maturity bonds of the same type. They should also be more rewarding (over the long-run).

Keep that guideline in mind because it’ll help you choose the right ETF once we’ve covered the bond risk-reward trade-off.

Now a bond ETF is diversified across a portfolio of bonds with many different maturities. As principal is repaid, the fund automatically reinvests that money in new bonds. (You can also choose to reinvest your interest payments, too.) The upshot is that a bond ETF normally expresses maturity as a range of years. For example, ‘7-10Y’. That means the ETF invests in bonds with maturities of 7 to 10 years.

justETF tip: You’ll typically see this figure mentioned in a government bond ETF’s name.

So just by scanning a bond ETF’s name you can intuitively grasp its level of risk and associated reward. The higher the maturity number, the higher the risk and the greater the potential return.

The task now is to work out your personal risk-reward sweet spot.

Choosing your spot on the maturity risk spectrum

ETF maturity figures can be helpfully summed up as short, intermediate, or long bonds like this:

Bond ETF maturity range (in years)

ETF holdings

0-5

Short bonds

5-10

Intermediate bonds

10+

Long bonds

Short bonds tend to be very stable – like cash. Long bonds can be very price volatile. At times they’ll be as wild as equities. Intermediates lie somewhere in-between. We’ll flesh out how they behave in a second.

justETF tip: Only make apples-to-apples bond maturity comparisons. For example, intermediate Euro government bond ETFs are riskier than short Euro government bond ETFs. But that doesn’t make the intermediate government ETF riskier than a short high yield bond ETF.

The bottom line is that longer maturity government bond ETFs experience greater volatility than shorter versions. That is, you’ll see a long bond ETF’s price fluctuate more in response to changes in interest rates, inflation, and other economic factors.

Remember we don’t want to endure much volatility on the defensive side of our portfolios so the simple answer is to choose a short government bond ETF and be done with it.

However, volatility can work for you as well as against. Nobody complains when our ETFs surge in price and this is a form of volatility, too. During a recession, longer-dated bonds may experience higher demand than shorter bonds because they’re often a better refuge during a storm.

Looking back at these moments of crisis helps us understand how bonds behave and why they’re worth owning.

Bond ETF performance during the Global Financial Crisis (GFC)

The chart shows how short, intermediate, and long bond ETFs helped when the GFC raged from 2007-2009:

iShares Euro Government Bond 15-30yr UCITS ETF (Dist)iShares Euro Government Bond 1-3yr UCITS ETF (Dist)iShares Euro Government Bond 7-10yr UCITS ETF (Dist) Lyxor MSCI World UCITS ETF (Dist)

Source: justETF Research, 27 November 2023

The grey line reveals the sharp decline of an MSCI World ETF during the crash.

The blue line shows how a short bond ETF could partially offset that loss by rising 9.4% at the peak of the crisis.

But the intermediate ETF (orange line) rallied 15.6%. Much better!

Meanwhile, the long ETF (red line) only managed a 9.6% increase. That’s marginally better than the short ETF but not enough to compete with its intermediate counterpart.

Theory suggests that the long bond fund should have won in this scenario but nothing works like clockwork in investing. Moreover, long bonds are especially vulnerable to price drops during periods of fast-rising inflation and interest rates …

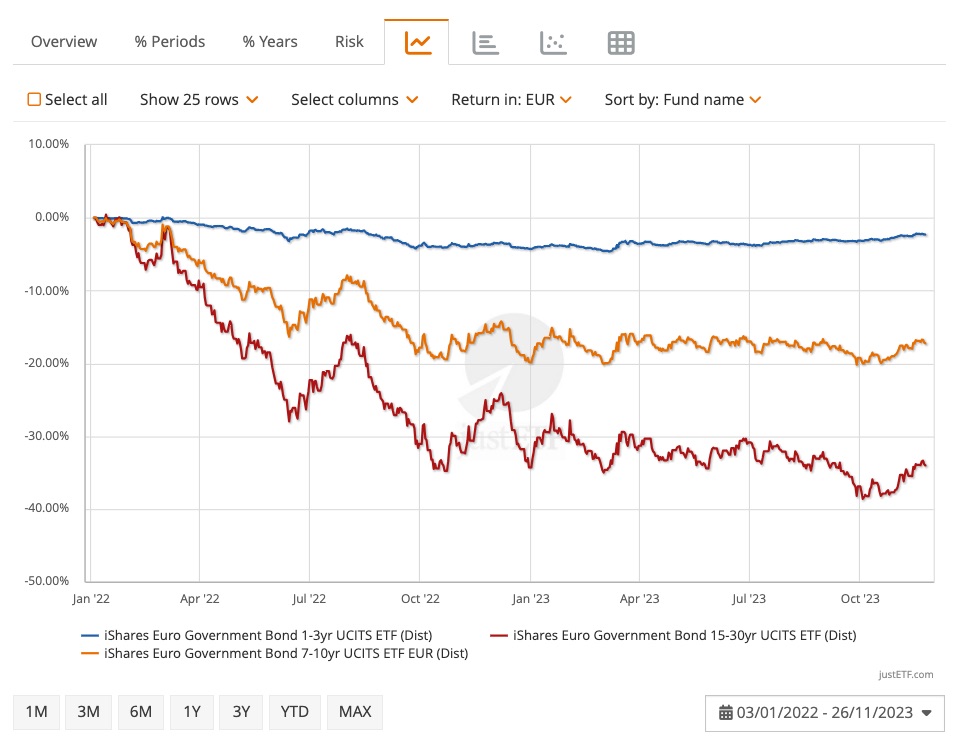

Now let’s look at the same trio of bond ETFs as inflation and interest rates escalated during 2022-2023:

iShares Euro Government Bond 15-30yr UCITS ETF (Dist) iShares Euro Government Bond 1-3yr UCITS ETF (Dist) iShares Euro Government Bond 7-10yr UCITS ETF (Dist)

Source: justETF Research, 27 November 2023

The short bond ETF (blue line) is down only 2.3% over the period. Short bonds are much less susceptible to inflationary conditions than longer bonds.

The intermediate bonds (orange line) fell -17%. This is an unusually large slide for a government bond ETF but it can happen.

But by far the biggest hit is saved for the long bonds (red line): a steep -34% slump.

This shows the dark side of long bonds. They can be severely punished during inflationary outbreaks.

The key takeaway is that long bonds can be especially risky at times. And they may not pay off as well as expected during stock market crashes.

Now let’s look at the final part of the bond risk-reward trade-off: long-term returns.

Bond ETF returns comparison

All three bond ETFs delivered a reasonable cumulative return for defensive assets but the pecking order is clear:

iShares Euro Government Bond 15-30yr UCITS ETF (Dist) iShares Euro Government Bond 1-3yr UCITS ETF (Dist) iShares Euro Government Bond 7-10yr UCITS ETF (Dist)

Source: justETF Research, 27 November 2023

As you can see, short bonds (blue line) gave up a fair chunk of return in exchange for their low volatility behaviour. The ETF’s cumulative result over the period equates to a 1.4% annualised return.

Risky long bonds managed (red line) a 2.4% annualised return.

But intermediate bonds (orange line) produced a 2.8% annualised return for almost half the risk of the long bonds.

Different time periods will produce different results, but the evidence suggests that long bonds may not be worth the risk.

If you’re convinced you’re better off investing in the short to intermediate end of the maturity risk spectrum then long bonds can be eliminated at this stage.

Putting it all together

Here’s a quick recap of the strengths and weakness of the three main bond maturity types:

Bond ETF maturity range

Pros

Cons

Short (0-5 yrs)

Less price volatile

Less vulnerable to inflation / rising interest rates

Good equity diversifier

Less beneficial in recession

Lower expected return over time

Intermediate (5-10yrs)

Beneficial in recession

Better expected return over time

Very good equity diversifier

Susceptible to inflation / rising interest rates

Quite volatile (typically much less so than equities)

Long (10+ yrs)

Beneficial in recession

Higher expected return over time

Very good equity diversifier

Highly susceptible to inflation / rising interest rates

Very volatile (equity-like at times)

With long bonds gone, your final choice depends on your investment goals and circumstances.

For example, an accumulating investor may decide that intermediate bonds offer a good balance of equity diversification and expected returns over the long run.

However, a retiree is more vulnerable to inflation and needs to be able to withdraw funds from their portfolio without worrying about significant capital losses. So they may prize the price stability of short bonds above all else.

If you want the best of both worlds, then you could always split your asset allocation between multiple bond ETFs – it all depends on your personal balance of risks.

Use our ETF screener to choose your bond ETFs

With the bond ETF essentials at your fingertips, you can quickly pull a suitable selection of products together using our data.

Go to our ETF Screener to select from every bond ETF available in Europe.

From the drop-down menu select:

(You can also choose a maturity figure of 3-5 for short bonds and 7-10 for intermediates.) Don’t worry about Bond Rating as all Euro government bonds are investment grade and above.

Choose Social / Environmental from the Bond Strategy dropdown if you wish.

Compare your selection

The screener will automatically put your chosen ETFs into a tidy comparison table for you:

Source: justETF Research, 27 November 2023

We’ve selected 7-10 year intermediate government bond ETFs in the example above. (Check out how to compare your ETFs using the method outlined in How to choose a global ETF. This process works just as well for bond ETFs.)

You can quickly snip your longlist down to a short list by culling:

New ETFs: any with less than 3 years of data

High costs: chop any ETFs with a TER significantly higher than the rest

Small fund sizes: ditch those below 100€ million

Currency hedged ETFs: we’re using Euro denominated funds only

From your shortlist, choose the bond ETF with the right blend of features for you. Don’t just choose the ETF with the best performance when there isn’t much to choose between them. Small variations are probably just noise.

Do use performance to weed out any ETFs that are significantly trailing the pack.

Finally, check out the justETF ETF profile page for your top two or three choices. Read the fund literature on each ETF’s homepage too.

Alternative bond ETF options

Global government bond ETFs

Global government bond ETFshedged to the Euro behave in much the same way as Euro government bonds.

The benefit is extra diversification: mostly in the form of US, Japanese, and UK government bonds. The downside is that hedged products normally charge more in fees.

If you choose the global route then make sure you select ETFs with EUR hedged in the name to guard against currency risk. ETF Screener dropdown settings:

All asset classes > Bonds

Region > World

Bond Type > Government

Maturity > As before

Currency Hedge > EUR hedged

Aggregate bond ETFs

Aggregate bond ETFs add riskier corporate bonds and municipal bonds to the government bond mix. Choose this option for the hope of a little extra return but know that you’re giving up some recession protection in exchange.

ETF Screener dropdown settings:

All asset classes > Bonds

Region > World

Bond Type > Aggregate

Maturity > As before

Bond Rating > Investment Grade

Currency Hedge > EUR hedged

Inflation-linked bonds

Finally, inflation-linked bonds are worthwhile as a second bond ETF due to their anti-inflation properties.

That said, inflation-linked bonds are not a perfect inflation hedge when yields rise steeply. And they’re generally not as effective during recessions as the normal government bonds we’ve covered above.

So please take the time to familiarise yourself with the strengths and weaknesses of inflation-linked bonds before investing.

ETF Screener dropdown settings:

All asset classes > Bonds

Region > Europe

Bond Type > Inflation-linked/li>

Maturity > As short as possible

A bond for life

OK, that’s a lot but hopefully this guide gives you the ammunition you need to search for your best bond ETF.

If you’re new to investing and still finding your feet then it’s absolutely fine to start with a short Euro government bond ETF. You can always update your choice later as your confidence grows.

Remember that diversification is the only free lunch in investing so just making the decision to pair your equities with a high-quality government bond ETF is already a great move.

Stay up to date

Free English newsletter including the latest news & knowledge about investing in ETFs.