Buffer ETFs offer a tempting proposition: the chance of stock market upside with less downside. That sounds great, so what’s the catch?

The catch is, you don’t get something for nothing. In this case, the cost of reducing your losses means your gains are capped too.

How does that actually work? And is it a good idea?

Let’s find out.

Buffer ETFs explained

There are various buffer ETF types, but they generally offer a proposition like this:

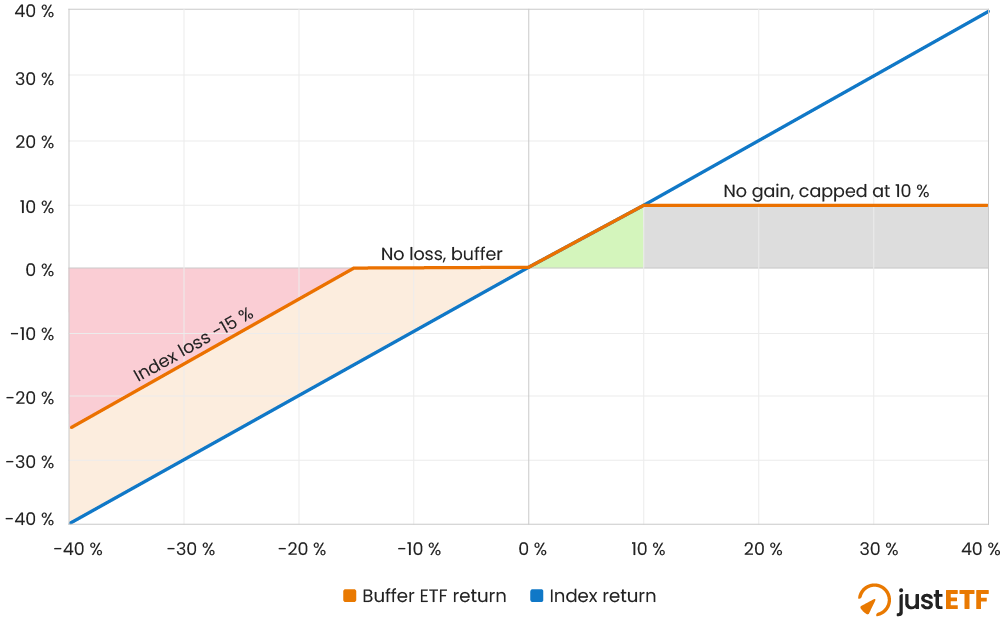

You are protected against some market losses over a specific length of time. For example, the ETF will shield you against up to 15 % of losses over the course of three months. This is the buffer.

In exchange, there’s a ceiling on your gains. For example, your buffer ETF returns will max out at 10 % over the period, even if its index rises much further. This is the cap.

The diagram below illustrates the idea:

Source: justETF

The buffer and cap mechanism illustrated above means that:

If the index comes in +8 %, your buffer ETF returns +8 %.

If the index delivers +30 %, your ETF is capped at roughly +10 %. You miss out on the remaining 20 % of gains.

If the index returns -10 %, your ETF is around 0 %, because the buffer has absorbed the loss.

If the index comes in -40 %, the first 15 % is buffered, but you take a hit after that: roughly -25 %.

So the trade-off is:

Less pain in downturns.

For less joy in strong up years.

Critical detail #1: The buffer and cap numbers only apply to a specific set of dates known as the outcome period. For example, the outcome period might run quarterly from the 1st April to 31st July or annually from 1st January to 31st December.

Critical detail #2: The cap and buffer numbers can look very different if you buy after the outcome period begins or sell before it ends. We’ll explain this more fully below.

Critical detail #3: Fees are deducted from your returns as per any other ETF. Therefore, you can still take a small loss after fees, even if the ETF’s index ends up in the buffer zone.

Critical detail #4: The cap and buffer are applied to the gains and losses of the ETF’s index - often called the reference index. We’ll talk more about this too.

The most important thing to understand about buffer ETFs

The buffer and cap behave approximately as advertised, only if you buy at or near the start of the outcome period and hold until the end.

But the headline buffer and cap numbers change if you buy later in the outcome period.

You can see this by visiting a Buffer ETF’s product home page.

Look for three key pieces of information. They will be labelled something like:

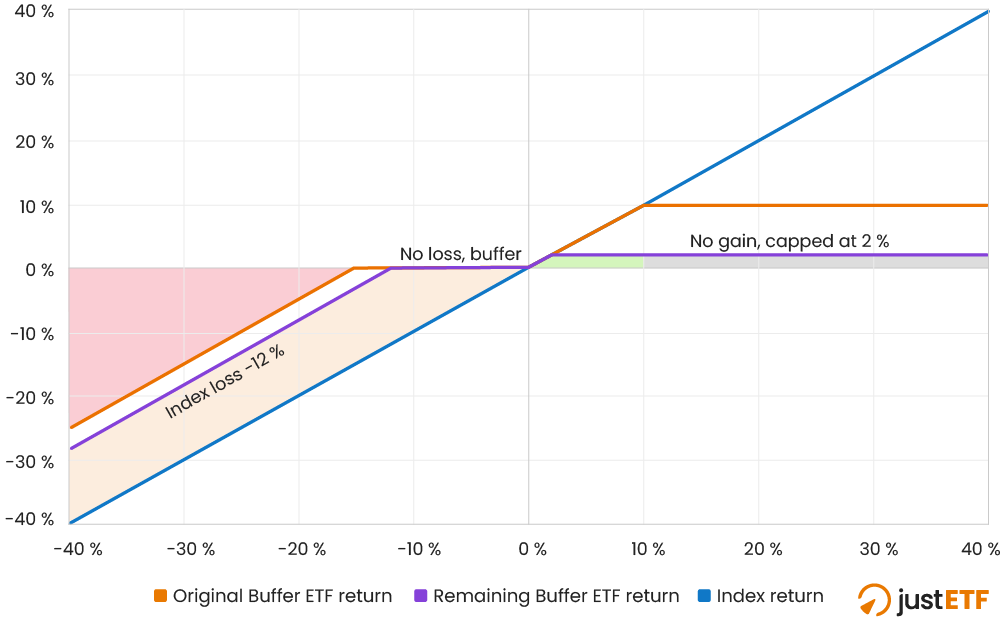

Remaining upside: This is the most you can expect to earn for the remainder of the outcome period before the cap kicks in. For example, the cap at the start of the outcome period may be 10 %, but the remaining upside may only be 2 % if you buy later on.

Buffer remaining: This is the maximum loss the ETF will absorb if you hold for the remaining outcome period. Perhaps the buffer was 15 % but will now only cushion you against 12 % of losses.

Potential loss before the buffer: This is the amount of loss you may take before the buffer protection even turns on. Again, this number is only a sound guide if you hold for the remainder of the outcome period.

Why would you take any loss before the buffer steps in? It could be because the index has already risen. Therefore - if you buy into the ETF now - the index has some distance to drop before it reaches the point where the buffer operates.

Also, the deal with some buffer ETFs is that you must eat a certain amount of loss before the buffer comes into play - even if you own them from the start of the outcome period.

Either way, the pay-off profile of the ETF changes as the time left in the outcome period declines. Here’s a simplified illustration of the remaining upside and remaining buffer we described above:

Pay-off profile of buffer ETFs

Source: justETF

That looks less appetising. Thus, the question to ask is from my entry point, how much can the ETF gain? How much buffer juice is left in the tank? And how far can the index drop before the buffer actually starts doing anything for me?”

What happens if I don’t hold for the entire outcome period?

We’ve been stressing that you need to hold for the full outcome period if you’re to enjoy the headline cap and buffer values.

But what happens if:

The index shoots up early in the outcome period? So there’s very little room left before you hit the cap: meaning you face a lot of downside risk without much upside remaining.

The index plummets early in the outcome period. Now you’ve got little buffer left, the economy is in recession, and the market could fall further, exposing you to losses.

In both circumstances, it could make sense to sell without waiting for the outcome period to end.

However, the prices you trade at may not reflect the changes in the index when you don’t hold the ETF from the beginning to the end of the outcome period.

That’s because, in scenario 1, the market could require a discount to buy an ETF that doesn’t have much upside remaining.

Or in scenario 2, buyers may demand a discount to cover the risk of buying a product that’s nearly exhausted its buffer.

The more time remaining in the outcome period, the greater the market uncertainty, the more likely it is that the ETF’s price will be discounted.

Whereas if you sold the same ETF with one day left to go, your result would more closely match the original buffer values - because buyers would be less nervous about the chance of a major market move against them.

Again, the above is an illustrative example. But it reflects the fact that the ETF’s price isn’t solely based on its index values. Market risk assumptions feed into the price too (among other factors) which is why Buffer ETF providers state that all given values are approximate, and rely upon holding for a defined outcome period.

Outcome period resets

Outcome periods are usually annual or quarterly. Once an ETF reaches the end of the period, it normally resets. (Check your ETF’s documentation to ensure that’s how it works.)

At the reset date, a fresh cap and buffer is established for the ETF.

However, the cap and buffer values may differ from the previous period.

So if you roll over a buffer ETF into a new outcome period, make sure you know what the new cap and buffer numbers are.

Do I earn dividends?

You don’t get dividends on top. Instead, you usually give up those cashflows to help fund the buffer structure.

That’s why buffer ETFs often track a price return index and not a total return index.

A price return index measures a market’s capital gains only.

A total return index counts capital gains and dividends.

If a buffer ETF references a price return index, then that’s a quick way to tell that dividends don’t add to your return.

Always read up on the index of any ETF you’re interested in. That will help you understand how the ETF works, what part of the market it covers, and if the product really is for you.

How do they protect against losses?

Behind-the-scenes, buffer ETFs take advantage of financial derivatives known as options to limit their downside.

The mechanics vary, but in brief they:

Get exposure to the index via a swap contract or through call options.

Buy put options that pay off if the index falls (think of this like insurance).

Finance those puts by selling other options, often:

Selling a put which sets the buffer size limit.

Selling a call that pays for protection by forgoing returns above the cap.

Obviously, such strategies involve more complex financial engineering than standard physical ETFs that invest in stocks.

Before investing, please read through a buffer ETFs’ documentation to understand the unique risks associated with options strategies.

Swap contracts have been used for years by synthetic UCITS ETFs to gain indirect exposure to various indexes.

This method entails counterparty risk: the chance that the swap provider defaults on its obligations to the ETF manager and therefore the product’s investors. Please read our counterparty risk primer to find out more.

Costs to consider

As previously mentioned, fees and other expenses reduce gains and add to losses. Buffer ETFs are complex, actively managed products and their TERs reflect this: ranging from 0.5 % to 0.9 %.

Other notable frictions beyond the TER include:

The cost of the options

The swap contract fee, if used

Additional transaction costs incurred by the ETF provider

Buffer ETFs are often promoted as a solution for anxious investors who struggle to handle even routine market losses.

Deeper risks can be managed by ‘Max Buffer’ type ETFs that absorb losses as high as 99 %.

‘Tail Hedge’ type ETFs expose the investor to moderate downside volatility, say the first 5 %, but then buffer the next 30 % of losses, for example.

Max Buffer and Tail Hedge ETFs in particular could suit near retirees who are a year or so from retirement.

In this case, an investor still wants the chance of some upside, but is more concerned with protecting their wealth from a large loss that could delay their retirement.

Traditional downside protection

However, it’s worth comparing buffer ETF pay-off profiles with cash and money market ETF interest rates.

Ultra-short term yields tend to be stable over limited periods, while extensive regulation and government protections mean that other downside risks are minimised.

Inflation is another threat, but the restricted upside of buffer ETFs means they’re more exposed to escalating consumer prices than normal equity ETFs over time.

Equity ETFs have historically beaten inflation by a large margin. Buffer ETFs are less likely to do so in the long run due to their capped upside.

Ultimately, buffer ETFs main attraction is the emotional comfort of reducing the chance of loss.

Just bear in mind that equities typically have more up years than down, and that volatility favours investors who can patiently cost-average over the long term.

As such, buffer ETFs are less likely to suit young accumulators, anyone who doesn’t take the time to understand the product’s complexities, people who want absolute guarantees, and investors who will kick themselves when they lag a plain equities ETF during a raging bull market.

Even buffer ETF enthusiasts acknowledge they’re best used as a satellite holding and shouldn’t replace your core positions.

To find more about the range of buffer ETFs available, go to our ETF screener > Equity Strategy > Buffer